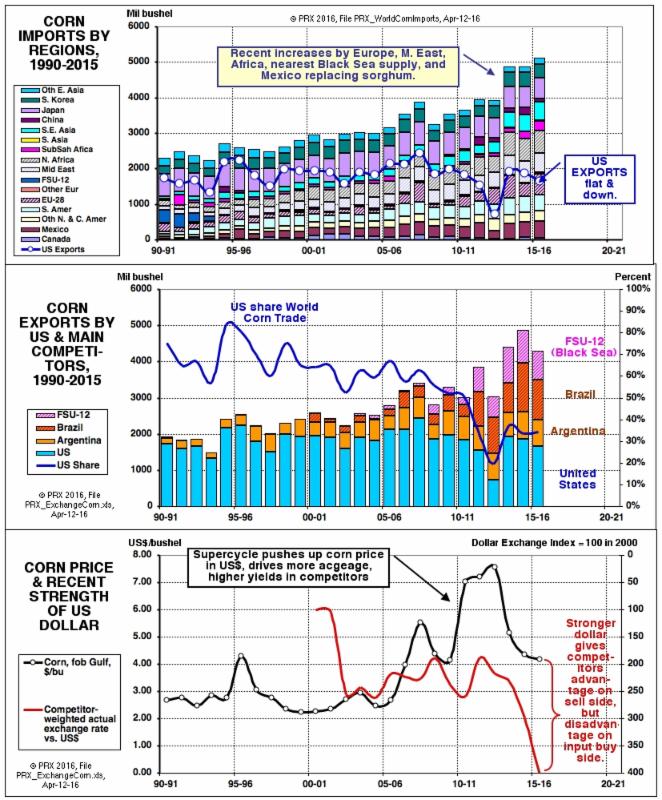

After World War Two, and through the period 1990-2005, the US share of world corn trade was usually well above 60 percent, frequently 70 percent or more. This dominance began to decline after 2007, and today the share is down to about 32 percent. The winners have been Brazil, Argentina, and the Ukraine/Russia Black Sea regions.

[1]

The top part of the figure below shows world corn imports by major buyers. It is noteworthy that in the past three crop years, world corn trade increased by over 1200 million bushels--about 250 million bushels to Mexico (replacing US sorghum shipped instead to China, about 600 million bushels more to Europe, the Mid East, and Africa (the regions nearest the cheaper Ukrainian/Black Sea corn), and the rest mainly to Southeast Asia (excluding China).

The middle chart shows the growth of the US competitors, who expanded dramatically after crop year 2007 or so, as the world corn price rose above $5.00 per bushel, and producers in South America and Ukraine quickly responded with more acreage, more fertilizer and other crop inputs, especially better seeds and more intensive practices. Corn yields of our competitors broke through old trends almost immediately, and are still decidedly up.

The bottom chart plots the corn price, along with a corn trade-weighted index of the strength of the dollar versus Argentina, Brazil, and Ukraine. Analysts frequently point to the rising dollar as the main culprit in the US loss of corn trade share, and I suppose this is mainly true--but it is a double-edged sword, as most farm inputs are priced in dollars, which penalizes our competitors on the production cost side.

Reliable and official data on relative costs of production per bushel of corn are available for the United States, but not for our competitors. But one or two factors are quite certain: The US has the highest cost of cropland by a wide margin, and we have steeper and steeper costs of rail and barge freight to move corn from inland states to ports. The farmland cost accelerated during the 2007-2013 "wealth build" in the cornbelt, and this high cost has always been a kind of "built-in feature" of an agriculture situated in the middle of the world's most prosperous and wealthiest country. Improving the cost and efficiency of the country's rail and barge "system" is the same kind of thing--our agriculture competes with environmental, recreational, and other political goals as in no other land on earth. It is true that American farmers have advantages in obtaining and using "high tech" crop inputs, but these have become increasingly expensive. The entire input cost side of the US corn-soybean sector grew by over $50 billion during the 2007-2013 wealth boom. Overall, it is clear that the US has no well-defined political goal of being the world's main future supplier of feedgrains and oilseeds.

We'll go over the recent transportation details of South American and Black Sea producers at the

May-18 Roundtable. Despite its political trauma, Brazil continues to make progress.

Recent short analyses in this series:

[1] Each of these three producers now has a "corn net export" capacity roughly the size of the US state of Illinois, in the range of 800-1200 million bushels, depending on annual weather. There is little soybeans or other oilseeds in the Black Sea, but the two South American competitors have vast supplies of soybeans, with still more Cerrado land available in Brazil.