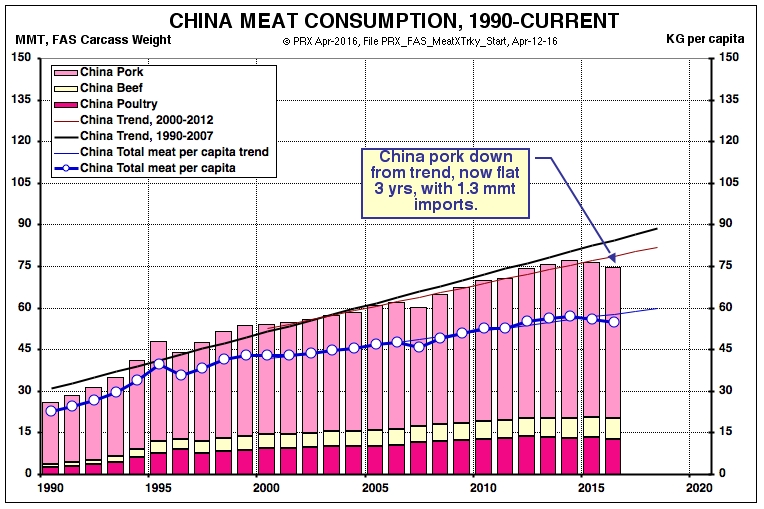

According to USDA's PSD international data system, world total consumption of all beef, poultry and pork comes this year to about 250 million metric tons, carcass weight. Of this, a little over 20 percent--about 54.6 mmt in 2016--is China pork. Ten years ago, China pork was 39.6 mmt, and two years ago in 2014 the number peaked at 57.2 mmt.

Most of China's 150 mmt of corn and other feedgrains goes to the feeding of pork, and most of China's imported 80 mmt of soybeans is used for meal to feed pork--along with (importantly!) vegetable oil for, let's say, a billion woks in which to cook this meat.

In other words, our strategic opinion on the future world demand for corn and soybeans is heavily dependent on what we think about China pork consumption. The chart below shows that the recent "glitch" in the growth of this market is noticeable, and worrisome--although we see another such dip in 2007 before growth returned to its upward trend.

The USDA's semi-annual China Livestock and Products Attache Report of March 5, 2016, "China's Pork Imports to Increase in 2016"

[1], explains the 2015 and 2016 downturn in terms of the recent rise in corn price supports, which have put stress on the profitability of hog operations, even as retail prices for pork have climbed to near record levels. The prospect for feedgrain costs to decline as the government changes the corn support policy (mentioned in a PRX analysis yesterday) has not had an immediate impact on pork output because of the shortage of investment money for pork producers and the build-up of environmental regulations on their facilities. This fits with what we read about an overall slowdown in China's economic growth and the many regional disparities in job opportunities now facing China's aggregate meat eaters. The Attache's emphasis on pork

imports (which will reach 1.3 mmt in 2016, mainly from Europe) adds a little more gloom on how long we can expect China's incredible volume of soybean imports from the Americas to continue growing. (Let me acknowledge that at this moment monthly shipments are holding steady with expected 2015-16 targets.)

One more feature of the overall landscape (and sea scape) deserves mention--and it's the guess we must all make about China's "global ambitions" vis-ŕ-vis the United States. It should be clear from news reports of China's military build-up and clashes in the South China Sea that the country's leaders have their own view about "global hegemony" and cooperation/dependence on the United States. In other words, buying lots of soybeans and grains from South America and the Black Sea is one thing--but depending heavily on the US cornbelt (for its "food security") is quite another!

This analysis is one of a series in the next days and weeks ahead of our May 18

PRX Roundtable, when we want to get our collective heads around the big picture, not only of meat demand, but increasingly I believe of the future need for BOTH meat demand and fuel demand ("food AND fuel"). We will find that the growth of paying world meat demand will continue to fall well short of our grain and oilseed productive capacity!