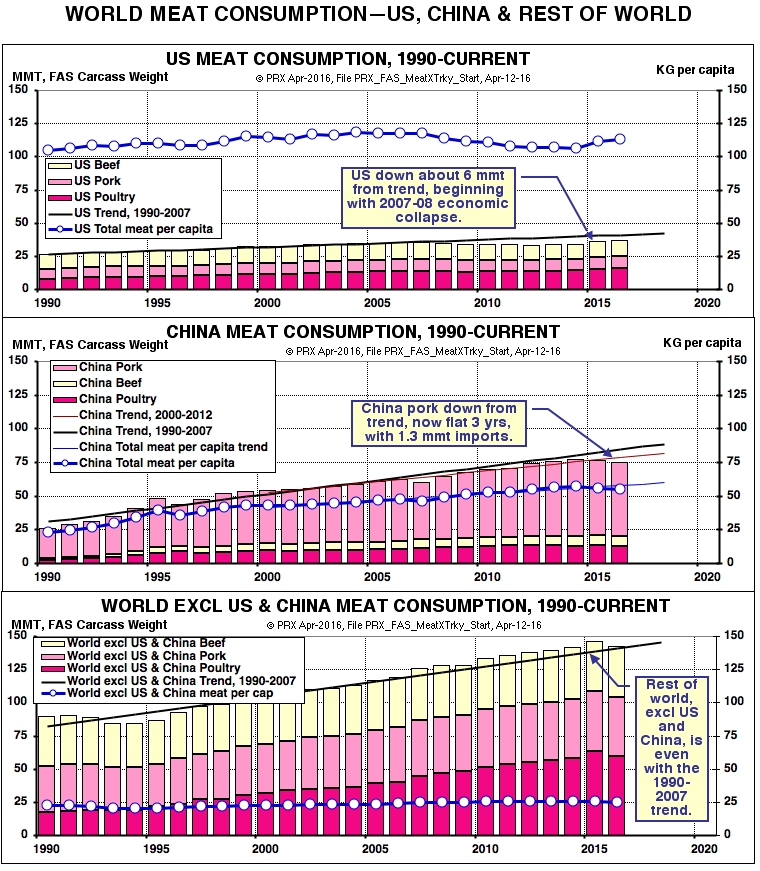

World consumption of beef, pork, and poultry in 2016 will total 253.6 million metric tons, carcass weight, per current USDA-FAS data. Of this, the United States accounts for 36.7 mmt, China for 74.7, and the Rest of the World excluding the US and China for 142.2 mmt.

The triple chart below shows the growth of these three regions since 1990. For the US, it is easy to see that its meat consumption declined sharply during the recent 2008-09 economic recession, that it has recovered somewhat since then, but that it does not show clear signs of returning to the former trend for quite some time. It may well be that Americans are "peaked out" on meat from the standpoint of health and other cultural concerns.

We discussed in the previous analysis of this series the present "glitch" in China's meat consumption growth, which the USDA China Attache attributes mainly to the country's policy "experiment" of very high rural subsidy prices for corn over the past five years, reducing the breakeven for hog producers, and raising the retail price of pork--all at the same time as a vast slow-down of growth for its export-oriented economy. Another "glitch" can be seen in China's meat use in 2007-09, after which the trend returns and increases somewhat. Altogether, the rise in China's meat consumption in the last quarter century has been extremely significant for world grain and oilseed prices and trade--and it can be best understood as an integral part of the one-time political-economic episode of China's joining itself to the world economy.

The third chart below, for the Rest of the World excluding the US and China, tells an important story in our quest for best commercial strategic thinking about corn and soybeans. Note that all three charts plot "total meat use per capita": 112.8 kg per person per year for the US, 61.8 for China, and 24.9 for the Rest--in 2016. Clearly, the average American eats twice as much meat as the average Chinese, and nearly five times as much as the average for persons elsewhere in the world. But note that annual consumption of 24.9 remains stable, despite the fact that

nearly two billion people were added to the Rest of the World from 1990 to 2016! In other words, to the extent that meat usage is an indication of "hunger" or not, the world did not get "more hungry" during this past quarter century. In fact, just the opposite.

[1] The often stated "truism" that another 2 billion people by 2050 will automatically stretch the world's grain and food production system to the breaking point is not proven by the facts so far.

Summary and Question. The aggregate statistics show that increasing meat consumption has been driven mainly by population growth, along with one staggering political-economic episode, namely the incorporation of a billion able and urbanizing workers in China (and elsewhere in Asia) to the world economy. We can see that US meat consumption growth is basically flat, but we can also see from the USDA data that meat consumption for the World Excluding the US is growing . . . at the rate of about 4.5 mmt per year. Is this rate fast enough to absorb the yield productivity gains ahead, along with the new farmlands still being added in South America? Over the next ten years, do we face shortage or surplus?

[1] See United Nations "State of Food Insecurity in the World," published May 2015, which reported that there are about 200 million fewer hungry people today than in 1990, meeting the goal of various UN projects and initiatives--again despite the addition of 2 billion mouths to the world, who are also "not hungry." This has much to do with gains in rice, wheat, and other foodgrain, as opposed only to feedgrains, oilseeds, and meat.