A much quoted essay by environmentalist Lester Brown in 1995 was entitled, "Who Will Feed China?" Brown claimed that with the (economic) rise of China, the job would become impossible--due to the country's lack of land resources, due as well to the lack of crop yield growth expected from biotechnology, and (most direly) to the prospect of Global Warming.

I published an analysis immediately in January 1996 disputing Brown's thesis. Today, of course, as shown in

Notes #1 and

#2, we know that the rise of China in the past 25 years has been spectacular, probably well beyond what Brown might have imagined, but that China has so far had no big problem with the job of feeding the country. By shifting rural population to urban, China has picked up some additional agricultural land (not really very much!), but where Brown erred the most was on yield growth from biotechnology--not so muchso in China, but in the World's Major Crop Export Hubs (the US, Brazil/Argentina, and to a lesser degree the Black Sea). Furthermore, although the

annual average temperature of the world has indeed generally increased, there has been no observable impact on crop yield trends, which for the global aggregate, for China itself, and most noticeably for the US and other Exporters continues up in straight line trends (with no increase/decrease in annual volatility).

In

Note #2 I said, "China is now 75% dependent on foreign imports of soybeans and palm oil for its basic food needs." Maybe the phrase "basic food needs" is a bit too broad, so let me narrow what I mean, and what can be readily calculated from official USDA and United Nations sources.

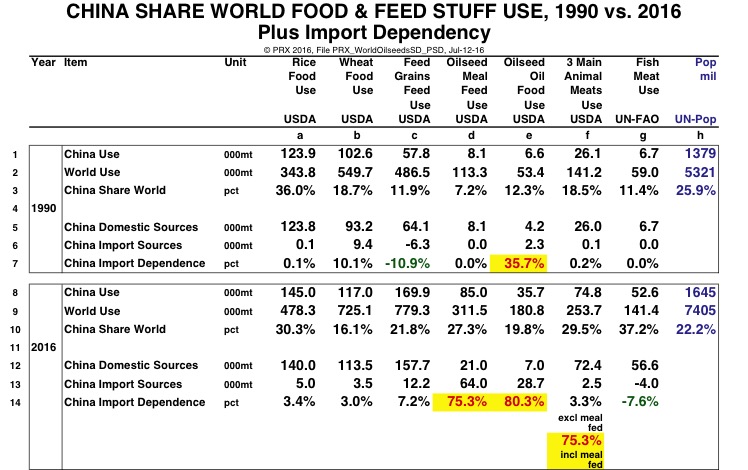

Take a look at the table below, which has columns for the food classes of rice, wheat, feed grains, oilseed meal, oilseed oil (i.e., "vegetable oil"), animal meats, and fish meat. The top seven lines deal with the picture of China's food use in 1990, and the bottom seven lines with the picture 25 years later in 2016.

In 1990, China's population was 25.9% of the world total population, and only in rice use did China exceed that percentage of world usage of a food class. Note that in one class, however, namely oilseed oil (the vegetable oil to cook foods in woks!), China was substantially dependent on imports, at 35.7 percent.

But in 2016, this oilseed oil dependency has increased to 80.3%, and the oilseed MEAL dependency (the processed vegetable protein fed to hogs, beef, and poultry) has reached 75.3%. This traded class is the 87 mmt/year of whole soybean imports, processed into meal and oil, along with other minor oilseeds, and also in the case of oil itself of processed palm oil from Indonesia and other neighbors around the South China Sea.

In the next couple of Notes, I'll zoom in on the oilseed meal and oilseed oil calculations and their 15 year history. Can the trends be sustained? Can/will China keep paying for ever-increasing volumes of oilseeds and/or meat? Will China's evident desire for regional "political hegemony" interfere with trade? Can North America and South America keep up with the demand? If the China demand growth so far has been so "incredible," why did the Global Price Super-Cycle collapse? Does another high price episode lie right around the corner?

Again, a reminder of the August 18-19 PRX Seminar, when we'll try to bring this all together in a single afternoon, with new crop risk management in a single morning! Early bird registration is here. View the agenda here.