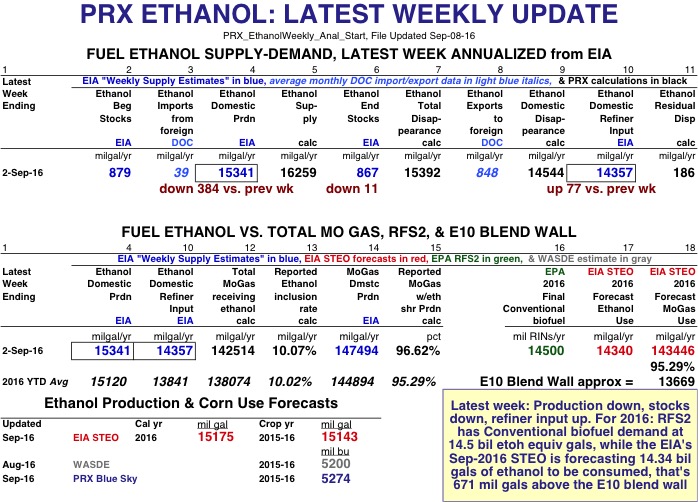

EIA Weekly Data: For the latest week ending 2-Sep-16, ethanol production was 15.341 billion gallons annualized, down 384 mil gals from the previous week--with a weekly residual error of 186 mil gals. Refiner input was 14.357 bil gals annualized, up 77 mil gals from last week, and the calculated inclusion rate for the 142.514 bil gals of mogas receiving ethanol was 10.07%. About 96.62% of all mogas (with 147.494 bil gals annualized) did indeed receive ethanol. Ethanol stocks were down 11 mil gals on the week to end at 867 mil gals.

Page 2 has PRX's calculation using EIA's weekly estimates and DOC import/export data for the 2016 year-to-date annualized average of ethanol domestic disappearance at 14.329 bil gals vs EIA's Sep STEO forecast of 14.34 bil gals. Yet, EIA's 2016 YTD annualized average of weekly estimates of domestic refiner and blender net input of fuel ethanol is only 13.841 bil gals, leaving a residual disappearance of 488 mil gals.

Page 3 has OPIS's last Friday 2016 RIN prices all down 4 cents or more this past week, except for D3 & D7 prices that were up 3 cents. As of yesterday, all 2016 RINs are up: D3 & D7 RINs are trading around $1.95, D4s are trading around 99 cents, D5s around 98 cents, and D6s around 88 cents. OPIS just started publishing 2017 future RIN prices that are trading around $2.35 for D3 & D7 RINs, $1.02 for D4s, $1.01 for D5s, and 88 cents for D6s.

Page 4 has JSA's Nebraska Group 3 ethanol margin up slightly this week to 51.9 cents.