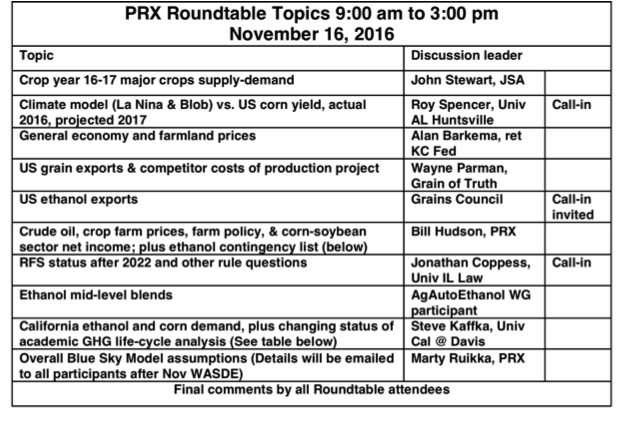

No matter who wins on November 8th, the uncertainties ahead for US soybeans and corn are enormous. After good US summer weather in 2016, the prospect of crop supplies returning to traditional surpluses and much lower prices seems likely, and a faltering La Nina may even favor bigger 2017 crops by competitors in South America.

But who knows about world weather!? We'll take a stab at this again, updating our La Nina/Pacific Warm Blob model, but the odds of forecasting future weather are VERY low--we do it mainly as a preview for clients of what opinions big money traders may take this winter (or not), especially those biased in favor of "steadily continuing, deleterious climate change."

What about demand, can't we say something more certain about that side of the table? Won't China continue to increase soybean imports by 3 to 4 mmt per year? Will the imports happen despite the "glitch" in official 2015-16 pork consumption numbers that we reported at our summer seminar August 18? Would continued strong imports be due mainly to China's absolute dependence on world markets for food oil, even moreso than protein meal? How long will China's urbanization and per capita food consumption keep increasing--unless its own domestic economy re-ignites? And what about corn? When will China stop subsidizing rural corn prices (in the range of $7 or $8 per bushel), and rely on cheaper world imports?

That brings us again to US politics! If we have a new Final Rule on the 2017 RFS from US-EPA before November 16, we'll present an analysis at the meeting. But whether the 2017 Rule is announced or not, the fact is that we are only five years away from 2022, when the "Annual Applicable Volumes" table in the 2007 Energy Act runs out, at which time we are left (fully!) to what the EPA decides the Volumes should be--unless, of course, Congress intervenes. Other contingencies for corn ethanol are shown here:

EXTENDED LIST of CORN ETHANOL CONTINGENCIES

- Continuation of RFS in current Law:

- After 2022, EPA reviews past implementation, makes joint analysis with DOE, USDA, and then sets new Applicable Volumes for future year(s)-with no min/max for "Total Renewable," thus no min/max for "Conventional"

(Max remains 15 bil gal???)

-

Could Life-cycle Analysis be changed by EPA? (Yes. Somewhat likely)

-

Could Congress re-visit RFS? Yes, of course. (Unlikely, before 2022)

- Could California strongly reduce midwest corn ethanol imports and/or corn for dairy in the next 5 to 10 years? (Unlikely, given the contined federal RFS)

- Could a Clinton Admin switch RFS to Calif style LCFS? (Not w/o Congress)

- Could Trump Energy Plan be implemented?

-

Revoke government regulations on all forms of US fossil fuels, cancel the Paris Climate Agreement, and stop all payments of U.S. tax dollars to U.N. global warming programs.

(Unlikely)

- Mid-Level Blends in 2020-22 and beyond, driven by CAFE?

- DOE and auto industry say must push for higher fuel-octane "floor," with fuels and engines designed as total system

- Vast efficiency gains (reduce mogas by 25 bil gal/yr), reduce GHG & BTX

- EPA says CAFE on track for 2022-25, and new fuels not part of this mid-term review-but okay after, depending on GHG reductions (Additional ethanol, between 5 and 10 bil gals, likely RINLESS)

Preliminary Agenda for November 16:

Origin of the PRX 10-Year "Blue Sky Model." The boom in ethanol dry milling began in 2004--with corn in surplus, with corn price very low compared to motor gasoline, and with dozens and dozens of announcements of new ethanol processing plants. These investments promised big profits, and the Energy Act of 2005 appeared to guarantee a "volume mandate" of 7.5 billion gallons, extended to twice that or more in the Energy Act of 2007. The proposed list of new construction topped 25 billion gallons! Was there enough corn for so many plants, and where should they be located?

The first run of the PRX Blue Sky Model appeared in 2006, covering the major US field crops through 2015. The Model was built at the state-by-state level, enabling transportation and cash price differential calculations--and providing extrapolation of county data for the PRX satellite-based origination mapping software used in many dozens of site selection studies.

The PRX Blue Sky Process today can be seen to differ dramatically from such academic modeling projects such as Purdue's GTAP, Iowa's and Missouri's FAPRI, and Texas A&M's FASOM. Most importantly, while the universities' audience is policymakers, the PRX Blue Sky aims strictly at commercial strategic planners and agribusiness investors and operators, mainly in the US corn and soybean sector. Policymakers--including the entire US federal government (which uses not only the university products but also such vast economteric models as the USDOE's Annual Energy Outlook)--seem impervious to the track record of these institutional forecasts compared to actual market realities, which to be polite but honest, is very, very poor.

PRX clients today include domestic and international grain merchandisers, ethanol processors, livestock feeders, input and seed suppliers, railroad and barge companies, agricultural banks, commodity groups (such as NCGA), and other profit-oriented agribusinesses. Our clients are well aware that "the future cannot be predicted," but they are equally convinced that "business requires good planning," and a key to success is forecasting and planning that is "a tiny bit better than one's competition."

The PRX Blue Sky Model relies on official crop and economic data from federal agencies, in most cases on historical series at the state-by-state level. But the aggregation, trending, and forecasting from this data--in Excel spreadsheets--is not automated by econometric or other statistical packages. The spreadsheets are controlled by a team of PRX staff with long exposure to commodity markets, who know that policy outcomes must be "guessed at" (not merely "held constant"), and who are eager to have the questions and opinions of other such people with "agricultural savvy." The main assumptions, and thus the entire model, are revised on average about four times a year. We are currently at Version 42, working on 43.

Finally, we are also beginning a new project on Cost of Production for our major export hub competitors, in South America and the Black Sea. Wayne Parman of Grain of Truth will update us on the progress with this critical new data.

Roundtable Meeting Limited to Ten PRX Staff and Outside Experts, plus Twenty PRX Clients. Location is the Argosy Casino Hotel, Kansas City, MO, 777 NW Argosy Casino Pkwy, Riverside MO, 816-746-3100, from 9:00 am to 3:00 pm Wednesday, November 16, 2016.

Boardroom setting accommodates max of 30 people, with emphasis on Q & A. Fee is $1,200. PRX room rate available for Nov-15 at $122 (includes buffet breakfast for direct hotel booking). Early arrivals welcome at informal PRX dinner at "Journey" restaurant in hotel, 7:00 pm on Nov-15. Working lunch also provided.

To register, or to put your name on future invitation list, contact chris@prxgeo.com.