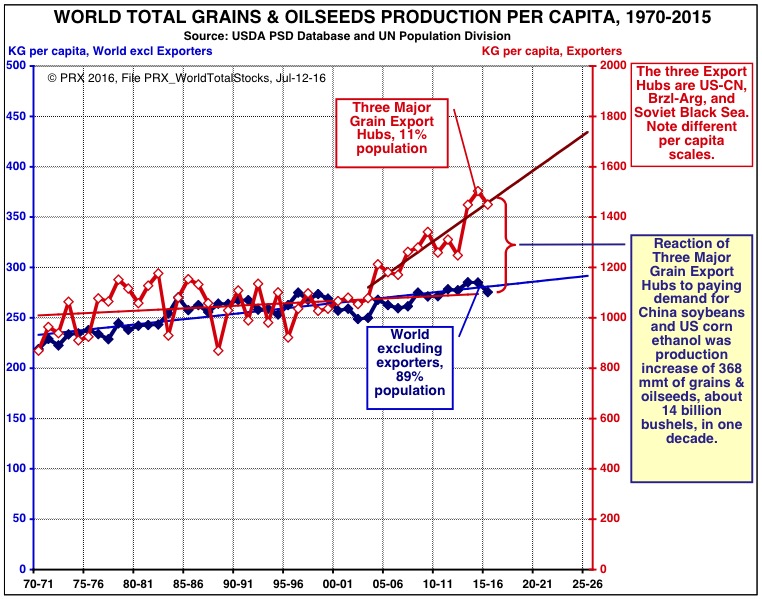

We have been using a number of "per capita" charts to capture the rise of China and its soybean import demand, so let me try to use the same display style on the supply side of the same episode.

The first chart below shows the kilograms per capita of total grains and oilseeds in two parts of the world--the three Export Hubs (on the right-hand scale), and the rest of the world excluding these exporters (on the left-hand scale).

Note Bene (Notice Well!). The right-hand scale is four times larger than the left hand scale. Every person living in the Export Hubs is associated with grain and oilseed production four times greater than every person in the rest of the world.

The reaction of the Three Major Grain Export Hubs to paying demand for China soybeans and US corn ethanol was a production increase of 368 mmt, about 14 billion bushels, in 12 years.

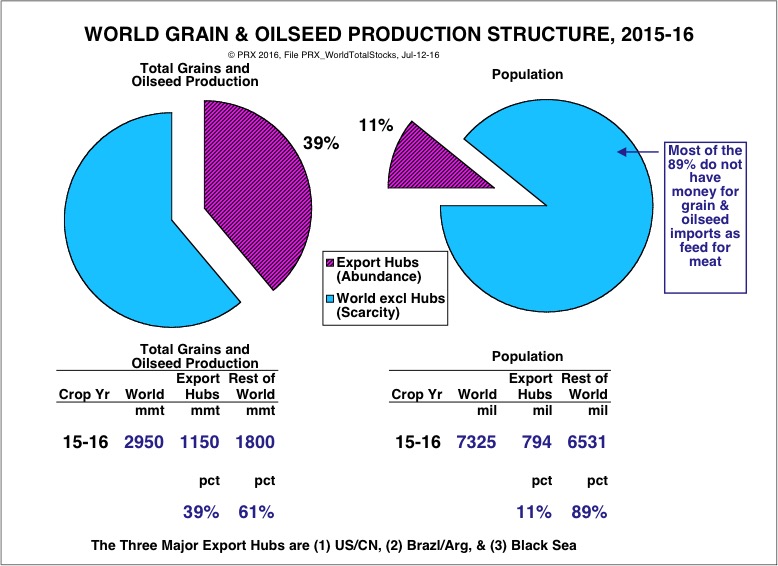

The second chart shows why this was possible: The Exporters have only 11 percent of the world's population, but 39 percent of the grain and oilseed productive capacity. The people in the Export Hubs cannot eat all these crops themselves, they must sell their surplus to other eaters in other lands, or they must use it for fuel.

This situation is a feature of the geographical resource distribution on the planet-soil and weather--but also (certainly in the USA) of prevailing political structure and overall industrial infrastructure. There is no other single agricultural resource on the globe like the American cornbelt--not even close!--and there are no more successful owners and operators of such a resource anywhere either.

[1]

Given continued decent weather into August 2016, both the US corn and soybean crops will be large, surplus stocks will build, and farm prices (now for two years at half the super-cycle peak of 2013) will decline further.

To overcome the "structural" grain and oilseed production advantage, the Export Hubs need demand from both food and fuel. The rise of China is a truly remarkable demand-side episode, but the surplus problem of the Export Hubs remains.

Early bird registration is here. Today (Friday the 29th) is the final day $200 early bird discount. View the agenda here.

[1] The US average corn yield is in the range of 160-170 bushels per acre. Corn contest winners can do 400-450 bushels per acre and more. The potential for further increase is vast.