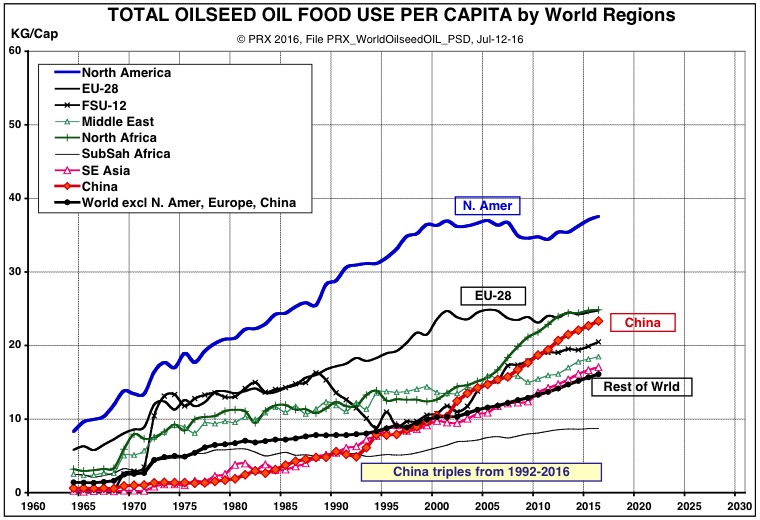

The first chart below shows that China's per capita use of vegetable oils for food has tripled in the past quarter century, coming close to that of the European Union--and not showing a decline in the past two years, as was the case with meat per capita.

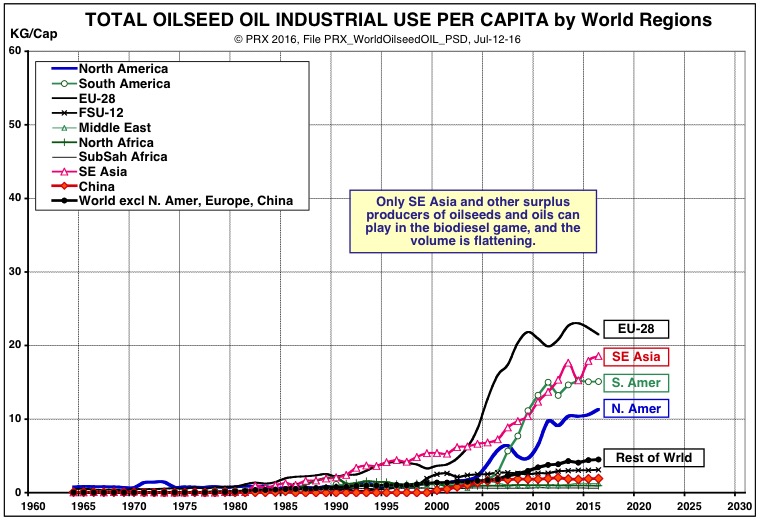

The second chart shows that China's per capita use of vegetable oils for fuel has not changed much at all in recent years, and that the big increases are in the surplus producers of oilseeds (North America and South America with soybeans, and Europe with rapeseed) and other oils such as palm oil (in Indonesia and the rest of Southeast Asia). The volume of the big biodiesel players is flattening, especially in the past year or more of lower crude oil price.

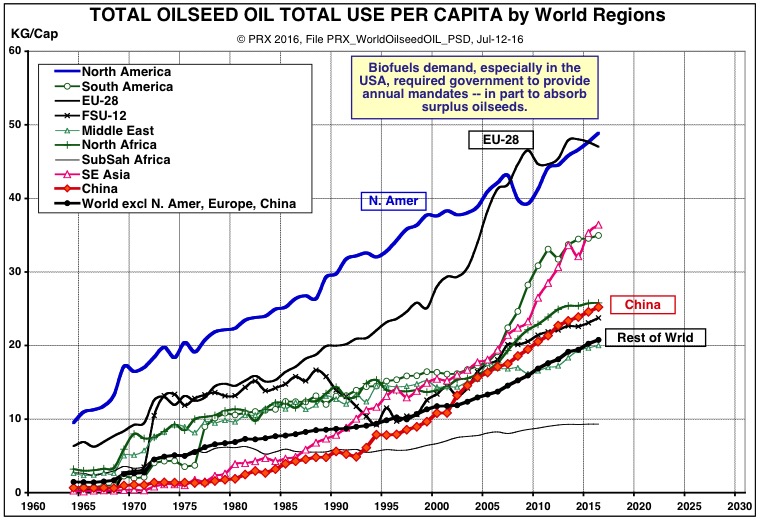

The third chart below shows the combination of food and fuel use (total use) per capita, with China above much of the world, but well below the major surplus producers of North and South America, Europe, and Southeast Asia. The biofuel policies of the USA and Europe have driven much of the biodiesel total demand worldwide, as especially the USA had surplus production capacity of soybeans and corn.

Question. What happens if China's economy weakens, or its politics becomes less friendly to the West, and/or if USA biofuel policies are less favorable to continuing the increased production for GHG reduction? Doesn't the RFS extend in law only until 2022?

Again, I'll venture an opinion on these important issues at the August 18-19 seminar. The next few notes will focus on China's supply side--can the country change its domestic crop patterns, or make other moves to counter its import dependency?

Early bird registration is here (only 3 days remaining for $200 early bird discount). View the agenda here.