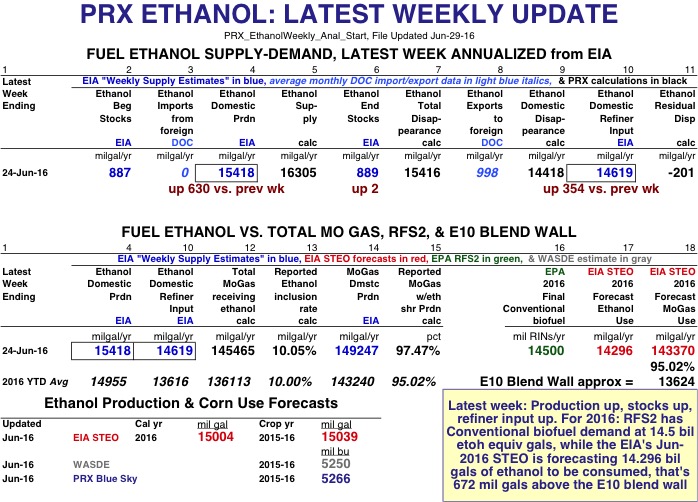

EIA Weekly Data: For the latest week ending 24-Jun-16, ethanol production was 15.418 billion gallons annualized, up 630 mil gals from the previous week--and with a weekly residual error of -201 mil gals. Refiner input was 14.619 bil gals annualized setting a new record high, up 354 mil gals from last week, and the calculated inclusion rate for the 145.465 bil gals of mogas receiving ethanol was 10.05%. About 97.47% of all mogas (with 149.247 bil gals annualized) did indeed receive ethanol. Ethanol stocks were up 2 mil gals on the week to end at 889 mil gals.

EIA's weekly import data survey showed about 7.64 mil gals of fuel ethanol imported over the past week, this is the first time the weekly data has showed ethanol imports in 2016. EPA's EMTS, that has data current as of June 10th, 2016, also reported for the first time 1.874 million importer generated D5 RINs, which are likely all advanced sugarcane fuel ethanol from Brazil.

Page 2 has PRX's calculation using EIA's weekly estimates and DOC import/export data for the 2016 year-to-date annualized average of ethanol domestic disappearance at 13.954 bil gals vs EIA's June STEO forecast of 14.296 bil gals. Yet, EIA's 2016 YTD annualized average of weekly estimates of domestic refiner and blender net input of fuel ethanol is only 13.616 bil gals, leaving a residual disappearance of 338 mil gals.

Page 3 has OPIS's last Friday 2016 RIN prices all rising over the past week, except for D3 & D7 RINs which were unchanged. As of yesterday, 2016 D3 & D7 RIN prices are trading around $1.77, D4's are trading around 92 cents, D5's around 89 cents, and D6's around 88 cents. RIN prices continue to rise as more market participants slowly realize that the RIN bank is likely going to be depleted in 2017.

Page 4 shows EIA's ethanol production jumping back up last week & JSA's Nebraska Group 3 ethanol margins fell 3.5 cents last week to 51.2 cents.