In the past few essays, we have calculated the annual increases in corn and soybean demand from increasing world meat consumption, and we have compared these annual amounts in millions of bushels with production and export trends of the three major World Export Hubs--the United States, Brazil & Argentina, and the Ukrainian Black Sea.

The three hubs by themselves, with only 11 percent of world population but with about 50 percent of the world's productive capacity for corn and soybeans, suffer from the "curse of agricultural abundance," as it was first called in the 1960s by Willard Cochraine, the USDA's Chief Economist under John F. Kennedy. The response at that time to persistent cheap grain prices was to transfer government monies to the American farm sector, using set-asides, loan rates, target prices, and other mechanisms.

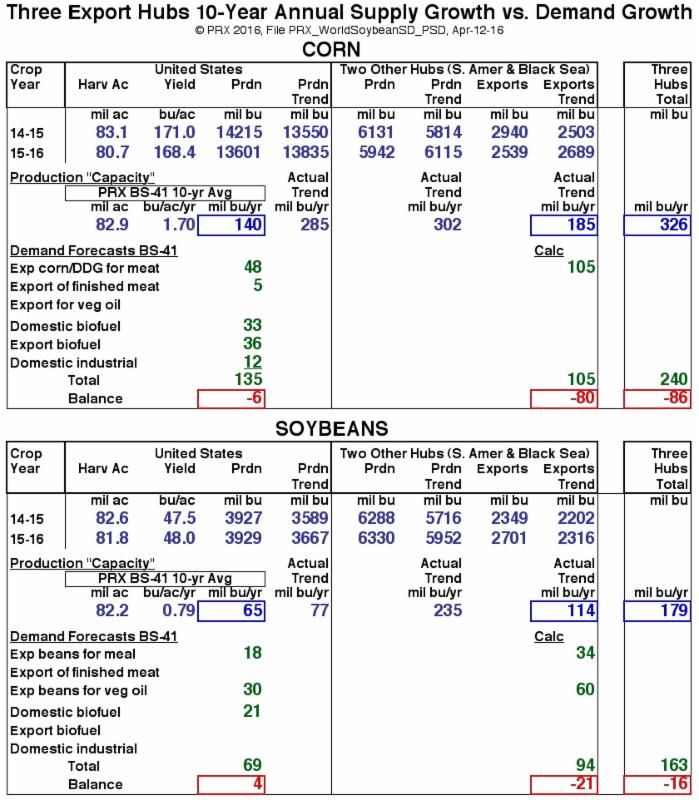

Most people today think in terms of our world in terms of grain and oilseed scarcity--but the truth (generated by simple geography) is just the opposite. The Three World Export Hubs are in enormous surplus. At least if the only or paying demand is for food and meat! That's my point with the table below, which compares a simple forecast of annual production capacity over the next ten years with a trend forecast of paying demand for increased meat consumption. The corn surplus is moreso than soybeans--due to another structural oddity, namely the political desire of China not to import corn from the United States, while at the same time buying vast quantities of soybeans mainly from South America.

As shown for the US, the corn supply growth balance versus demand is close to neutral (-6 million bushels per year), provided that 33 + 36 + 12 = 81 million bushels per year will come from new fuel and industrial demand in the next ten years. This would mean modestly expanded domestic usage of greater than E10 blends, plus greater finished ethanol exports, plus various new industrial uses (such as plastics). But note that the other two Hubs besides the US do not have the domestic fuel and industrial markets (e.g., no multi-billion gallon dry mill industry), and so the combined corn "balance" for all Three Hubs is -86 million bushels per year. The downward pressure on corn farm price would be felt on the US as well as Argentina/Brazil

[1] and the Black Sea.

The soybean balance picture is much stronger--so long as China continues to neglect its own soybean area and yield, in favor of 80 mmt plus imports of whole soybeans every year, providing not only meal for pork meat but half the vegetable oil needed in which to cook this meat!

Key Question. How likely is it that higher crude oil prices and favorable US corn ethanol policies will sustain the balance we've calculated for corn, or is it possible that America's "surplus corn curse" could be defeated by even higher energy prices and sounder biofuel policies that what we now have?!

Reminder of the PRX Strategic Roundtable, May 18 in Kansas City, when our staff, outside experts, and many key clients will debate the whole subject of future biofuel demand! Agenda is

here.

[1] Argentina has recently announced its intention to blend more ethanol domestically, and of course Brazil began decades ago blending large volumes of sugarcane ethanol into motor gasoline. But Brazil's sugarcane ethanol has little to do with its own corn market structure, and in fact--because US biofuel policy declares sugarcane ethanol an "advanced biofuel"--the potential exists for sugarcane biofuel imports to displace US corn biofuel demand, especially in the billion-gallon market of California.