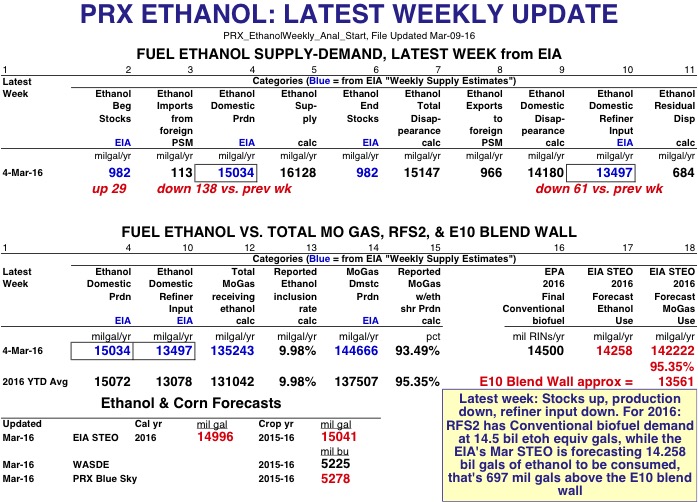

EIA Weekly Data: For the latest week of 4-Mar-16, ethanol production was 15.034 billion gallons annualized, down 138 mil gals from the previous week--and with a weekly residual error of 684 mil gals. Refiner input was 13.497 bil gals annualized, down from last week, and the calculated inclusion rate for the 135.243 bil gals of mogas receiving ethanol was 9.98%. About 93.49% of all mogas (with 144.666 bil gals annualized) did indeed receive ethanol. Ethanol stocks were up 29 mil gals to 982 mil gals.

EIA's March STEO is forecasting 2016 ethanol production at 14.996 bil gals, of which 14.258 bil gals is forecasted to be consumed in motor gasoline. It's also forecasting 2016 motor gasoline consumption at 142.222 bil gals.

The March WASDE kept 15-16 corn for ethanol production at 5225 million bushels, while PRX's Blue Sky model has it at 5278 mil bu.

Page 2 uses EIA's weekly estimates to calculate 2016 year-to-date annualized average of ethanol domestic disappearance at 14.219 bil gals, which can be compared to EIA's March STEO forecast of ethanol blended into motor gasoline at 14.258 bil gals. However, EIA's 2016 YTD annualized average of weekly estimates of domestic refiner and blender net input of fuel ethanol is only 13.078 bil gals, leaving a residual dissappearance of 1.14 bil gals.

Page 3 has OPIS's last Friday 2016 RIN prices all falling a few cents and holding fairly steady this week. As of yesterday, D6's are trading around 72 cents, D5's 76 cents, and D4's 77 cents. OPIS started publishing 2015 & 2016 Cellulosic (D3 & D7) RIN prices at the beginnning of March. The 2015 & 2016 Cellulosic RINs are currently trading around $1.34 & $1.83, respectively. These RINs are valued more than the 2015 & 2016 Cellulosic Wavier Credits of 64 cents & $1.33 because they can be used to satisfy obligated party's advanced and renewable fuel obligations, along with being traded, sold, or banked.

Page 4 has JSA's Nebraska Group 3 ethanol margins up 3.3 cents last week to 31 cents.