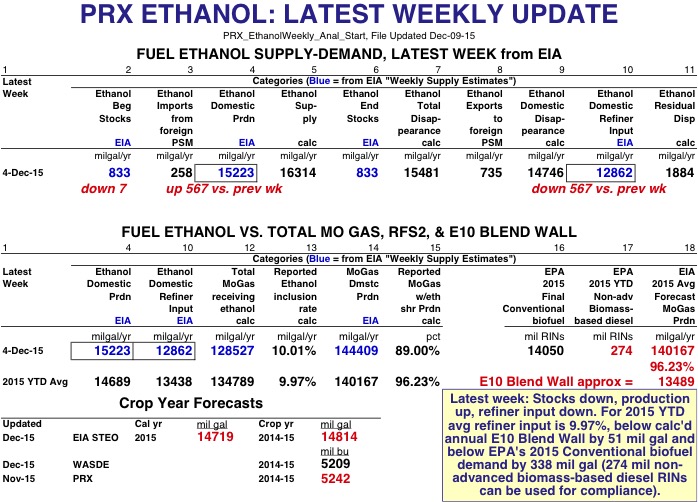

EIA Weekly Data: For the latest week of 4-Dec-15, ethanol production was 15.223 billion gallons annualized, up 567 mil gals from the previous week--and with a weekly residual error of 1.884 bil gals. Refiner input was 12.862 bil gals annualized, down 567 mil gals from last week, and the calculated inclusion rate for the 128.527 bil gals of mogas receiving ethanol was 10.01%. About 89% of all mogas (with 144.409 bil gals annualized) did indeed receive ethanol. Ethanol stocks were down 7 mil gals to 833 mil gals.

EPA's Final Rule has 2015 Conventional biofuel demand at 14.05 bil RINs. EIA's 2015 YTD average ethanol domestic refiner input is 13.438 bil gals, which is the equivalent of 13.438 bil RINs. Thus, 612 million more RINs are needed to fill this conventional biofuel demand in 2015. 274 mil non-advanced biomass-based diesel RINs generated from Jan to Oct 2015 will likely be used, leaving 338 mil RINs that need to be retired for compliance in 2015. This extra demand will likely come from more ethanol blending and non-advanced biomass-based diesel blending; however, it can also be filled by any advanced biofuel or carryover RINs from last year.

EIA's December STEO is forecasting 2015 ethanol production at 14.719 mil gals and has crop year 14-15 production pegged at 14.814 mil gals.

The USDA December WASDE kept crop year 14-15 corn for ethanol production at 5.209 billion bushels and increased 15-16 use 25 million bushels from last month to 5.2 billion bushels.

Page 3 has OPIS's last Friday 2015 RIN prices jumping following EPA's release of the Final Rule. RIN prices have cooled off a little following their initial surge after the release of the new rule. Yesterday's 2015 D6 RINs traded around 65.5 cents, D5's 72.5 cents, & D4's 72.25 cents, narrowing the D5/D6 spread to 7 cents.

Page 4 has JSA's Nebraska Group 3 ethanol margins falling 1.5 cents last week to 33.7 cents. It also has EPA's Final Rule for 2014 Conventional biofuel demand at 13.61 bil gals, 14.05 bil gals for 2015, & 14.5 bil gals for 2016.