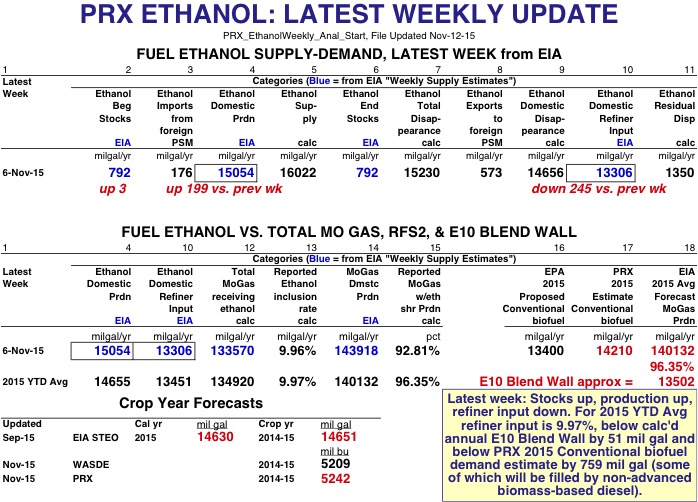

EIA Weekly Data: For the latest week of 6-Nov-15, ethanol production was 15.054 billion gallons annualized, up 199 mil gals from the previous week-and with a weekly residual error of 1.35 bil gals. Refiner input was 13.306 bil gals annualized, down 245 mil gals from last week, and the calculated inclusion rate for the 133.57 bil gals of mogas receiving ethanol was 9.96%. About 92.81% of all mogas (with 143.918 bil gals annualized) did indeed receive ethanol. Ethanol stocks were up 3 mil gals to 792 mil gals.

EIA weekly fuel ethanol imports, all to the west coast, were 7.644 mil gals last week, up from 2.94 mil gals the previous week. These imports all likely came from Brazil and took advantage of the D5-D6 RIN spread, the Carbon Intensity Point advantage Brazilian sugarcane ethanol has over US corn/sorghum ethanol, and the strength of the US dollar.

Page 3 has OPIS's 2015 Friday RIN prices all rising a few cents from last Friday's prices and continuing to rise this week. OPIS in now publishing 2016 RIN prices and EPA released last week the 2016 Cellulosic Wavier Credit (CWC) price at $1.33/RIN. Click here to see how EPA calculated the 2016 CWC price. PRX is forecasting the 2017 CWC price at $1.84/RIN, but this forecast will change as the actual data becomes available.

Page 4 has JSA's Nebraska Group 3 ethanol margins falling 3.8 cents last week, down to 36.5 cents and back up this week to 40.3 cents. It also has revised PRX estimates for Conventional biofuel demand that is likely to be released in EPA's Final Rule: 13.6 bil gals for 2014, 14.21 bil gals for 2015, & 14.38 bil gals for 2016.

Ryan Ruikka

Energy Analyst

The ProExporter Network

114 S. Main St. Suite 100

Chelsea, MI 48118

Off: 734-475-0454

Fax:734-475-0452

|