Progress in Basic Understanding. At last year's PRX Annual Seminar in March 2014, I presented a view of world grain trade dominated by "Three Export Hubs" (in surplus) vs. "Rest of the World" (in deficit). In fact, the Hubs have only 13% of world population, but 39% of world grain production. This geo-structural feature of our planet is why grain, in the Hubs, is "born cheap." Unless a large portion of the rest of the world has money to buy food/feed from the Hubs, demand is lacking and price is low. Or unless new uses for the surplus, such as fuel rather than food/feed, is found for the grain.

In December of 2014, I published a detailed report, "US Corn-Soybean Sector Wealth Build 2007-2013," explaining that in these seven recent years an all-time explosion of net income--over $200 billion-had erupted in cornbelt. The money amounted to more than an extra million dollars for every 1,000-acre corn-soybean farm in the country. The money was welcomed by farmers, of course, but its true source was not completely obvious. I traced how 16% was due, in an accounting sense, to corn ethanol grind, 12% to soybean exports to China, 27% to corn and beans to other export destinations, and the remaining 45% to other domestic uses.

Episodes vs. Long-Term Trends. At this year's August 2015 Seminar, I will present a detailed defense of the view that the above Wealth Build 2007-2013 was driven by a "global commodity price super-cycle" that relied on speculative investment in a basket of commodities (including corn and beans), and on capital sources transferred to the commodity sector from elsewhere in the world economy.

In the past six months of explaining these ideas to clients, I have discovered a number of key conceptual blocks to accepting the PRX approach. The most stubborn of these is the disreputable image many of us have of "speculation and speculators." The professional economists among us all insist that "supply-demand fundamentals" drive the entire show.

But the recent "commodity price super-cycle" is now clearly over. It was an episode, laid atop various familiar trends-but a feature of economic life with a beginning, a middle, and an end. A seven-year story, if you will, with characters and a plot we can now discern. Were its elements disreputable, or simply real? (By the way, though the episode was unexpected, it was not a random Black Swan!)

As we read today in the financial press. "The shift [in the value of the dollar] will do little to ease concerns that the global economy is slipping, raising doubts about commodities' value as an investment class." (WSJ, 7-21-15.) Further, says the Journal, one chief investment officer at a private bank, which manages $68 billion, "has cut all commodity exposure out of his portfolio." So have you asked your local bank whether they, or their headquarters, speculates in commodities? Does calling commodities an "investment class" remove the old onus of "sheer speculation"?

PRX Theory in Words of a Long Time Grain Trader (John Stewart)

- Cash corn prices are very strongly influenced by corn futures prices, which are primarily influenced by speculators whose trading volume dwarfs that of producers.

- This can be a good thing or a bad thing for producers. The high prices we have experienced for several years [2007-2013] were attributable to large speculative long positions.

- Crude oil is one of the key commodities that influence and fund large speculators. They see this as an indicator of inflationary expectations, and, rightly or wrongly, these traders, who control very large amounts of money, will buy a basket of commodities.

- Grains, including corn, were part of this basket, and this is why we have used the crude oil price in our Blue Sky corn regression model--and, up to now (!), it has greatly improved the fit.

- Taking the same positions, long or short, in all of the commodities in a basket of commodities helps explain the so-called "co-variance" of commodity prices.

- Flows of money in and out of the entire basket can raise (or lower) individual commodity prices without any correlation to change or lack of change in the underlying supply/demand fundamentals.

- Large (spec) traders may have an opinion of the supply/demand fundamentals of a given commodity, which could agree with the trade consensus or even with the views of the Chief Economist of USDA, but the positions they take may appear contradictory.

- The US CFTC issues a weekly Commitments of Traders report that details the futures positions of various classes of traders. Comparing the size and changes in these positions in reaction to changes in supply/demand fundamentals and economic and political developments can often provide clues about likely highs and lows in some commodities.

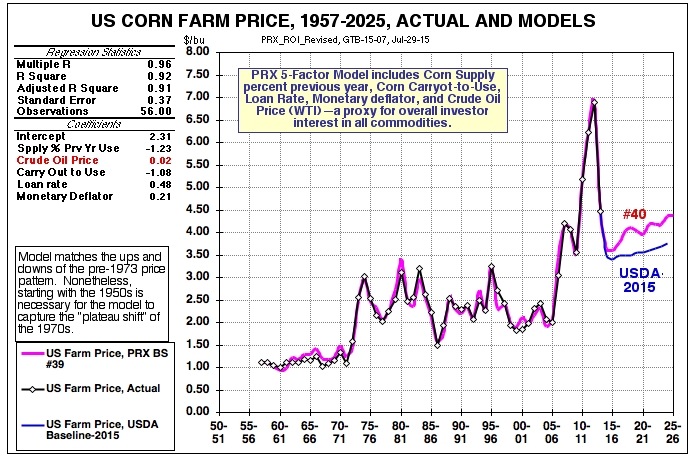

The chart below shows the PRX Blue Sky corn farm price model since 1958. The R-square fit of 0.92 is dazzling--and dependent on the use of crude oil price as a proxy for outside speculative interest in commodities, along with such well-known independent variables as the corn carryout-to-use ratio.

Let me emphasize that the "theory" elucidated above by John Stewart is as crucial to the short-term trade advice provided by JSA to merchandisers as it is to PRX long-range outlooks. As regular attendees know, every seminar is divided one afternoon to longer term and one morning to old and new crop cash, futures, and spreads issues.

In preparation, if you have done so, I recommend that you study the last PRX Quarterly Report and Podcast here. Seminar registration is here.