|

Slower Growth Ahead

Weekly Update - April 29, 2013

|

|

|

In This Issue

|

|

|

|

|

|

The Markets:

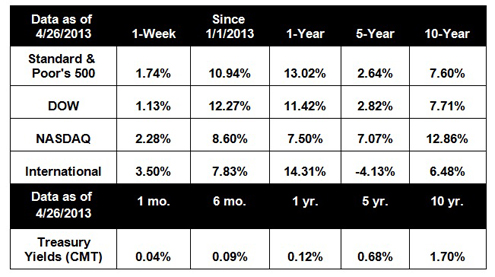

Markets ended positive last week despite a disappointing GDP report, erasing losses endured the previous week. As of Friday's close, the S&P 500 gained 1.74%, the Dow climbed 1.13%, and the Nasdaq increased 2.28%.[1]

Earnings data and a handful of economic reports drove most of the market action last week. According to our first peek at preliminary first quarter GDP data, the economy grew at an annualized rate of 2.5%, which is up significantly from the 0.4% gain in the fourth quarter of 2012, but still below consensus expectations of around 3.0%.[2] While the data is preliminary, a deeper look suggests we may face slower growth in the second quarter. Let's break down the numbers to see why:

Nearly all the gains in Q1 came from consumer spending and inventories. Consumer spending is expected to drop in the spring as Americans continue to feel the effects of the 2% payroll tax increase. Inventory growth, driven by farmers stocking up their silos after last year's drought, made a strong contribution to last quarter's growth; however, the activity was unusual, and unlikely to continue into Q2. Furthermore, government spending, which accounts for a significant part of economic activity, is declining rapidly - dropping 4.1% in Q1 alone. Most analysts expect government spending to continue to slide as the effects of sequestration become more pronounced.[3]

On the earnings front, more than 30% of the S&P 500 has reported and, while results are uneven, the news is mostly good. Blended earnings are up 2.4% in the first quarter, which is great since most analysts had low expectations. Two standout sectors thus far are technology, which benefited from strong consumer electronics sales, and building materials, which is getting a boost from the housing sector.[4]

On the downside, there are a lot of revenue misses happening; so far, only 39% of companies have beat revenue expectations, which is far below the historic average of 61%. This indicates that demand is still soft and companies are achieving their results by cutting costs. Anemic revenue growth seems to be tied to slow global demand, which is a particular problem for large multinational corporations that do a lot of business abroad. Demand in Europe is essentially flat, and sales volume is down across the board, making it difficult for companies to improve their margins.[5]

Next week will see the release of a slew of economic data, along with the steady march of more earnings reports. Analysts will be closely watching consumer spending and consumer confidence data, as well as the jobs report to see whether more market upside is possible. As always, we'll continue to monitor earnings reports and economic data and keep you updated.

ECONOMIC CALENDAR:

Monday: Personal Income and Outlays, Pending Home Sales Index, Dallas Fed Mfg. Survey

Tuesday: Employment Cost Index, S&P Case-Shiller HPI, Chicago PMI, Consumer Confidence

Wednesday: Motor Vehicle Sales, ADP Employment Report, PMI Manufacturing Index, ISM Mfg. Index, Construction Spending, EIA Petroleum Status Report, FOMC Meeting Announcement

Thursday: International Trade, Jobless Claims, Productivity and Costs

Friday: Employment Situation, Factory Orders, ISM Non-Mfg. Index

|

|

|

|

Performance

Notes: All index returns exclude reinvested dividends, and the 5-year and 10-year returns are annualized. Sources: Yahoo! Finance and Treasury.gov. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Notes: All index returns exclude reinvested dividends, and the 5-year and 10-year returns are annualized. Sources: Yahoo! Finance and Treasury.gov. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

|

|

Headlines:

Durable goods orders dropped in March. Orders for long lasting manufactured goods recorded their largest drop in seven months, falling by 5.7% in March, following a 4.3% increase in February. The drop was nearly double what economists had expected, and indicates factory activity may be cooling off.[6]

Unemployment claims drop. The number of Americans filing jobless claims fell by a surprising 16,000, showing a possible improvement in the job market. The four-week moving average, a less volatile gauge, also fell, easing concerns of deterioration in labor market conditions.[7]

Oil, gasoline prices fall. The price of crude oil slipped last week as first quarter GDP growth came in under expectations. Coupled with disappointing economic growth in China, this report left analysts wondering if global demand for oil will soften in 2013. At the pump, the average price of gasoline dropped to $3.51, down 32 cents from a year ago.[8]

Spain delays deficit targets. In an admission that its severe austerity measures had failed to control its finances, Spain slashed its economic forecast and extended its deficit targets by two years. Economists warned that Spain's economy would contract by 1.3% in 2013, but might grow by nearly half a percent in 2014. As anti-EU sentiment grows in core nations like Germany, these delays may make it politically difficult to continue to bail out countries like Spain.[9]

|

|

|

|

"Doubt whom you will, but never yourself."

- Christian Nestell Bovee

|

Pesto Pasta Salad

This tangy, healthful pasta salad is perfect for a weeknight dinner. Recipe from RealSimple.com.

Ingredients:

1/2 cup whole-wheat pasta

1/2 cup arugula

1 tablespoon pine nuts, toasted

2 tablespoons thinly sliced sun-dried tomatoes

2 tablespoons pesto

1 tablespoon goat cheese, crumbled

Directions:

1) Cook the pasta according to the package directions. Drain, rinse under cold water, and transfer to a medium bowl.

2) Add the arugula, nuts, tomatoes, and pesto and toss. Transfer to a plate and top with the cheese.

|

Get a Good Grip

Good golfers always have a solid grip on the club. To start, grip the club with your gloved hand and keep the handle's placement in the fingers between the first knuckle and the palm. Then, wrap your ungloved hand comfortably around the handle. From there, the thumb and index fingers of both hands form two V's - both of which should be pointed somewhere around the right side of your chest or right shoulder.

|

|

Broaden Your Horizons

Travel somewhere you've always wanted to go! Whether it's across town or the other side of the world, traveling is a great way to expand your horizons. Research shows that extending your comfort zone, engaging in stimulating new activities, and learning a language increase mental acuity. If you feel a little intimidated about traveling, seek out organized tours or group activities based on your interests.

|

|

|

| Use Regular Household Supplies as Cleaners

Replace expensive, specialized cleaning products with regular, everyday items and save some money in the process:

Use ketchup to remove tarnish from brass and copper goods. Squeeze it on a cloth and rub it in. The acidity from sugar and tomatoes works to remove tarnish without harsh chemicals.

Use glycerin (available from the pharmacy section of any grocery store) to remove dried wax from candlesticks, tablecloths, and wood furniture. Peel off as much wax as possible, then moisten a cotton ball with glycerin and rub until clean.

|

|

|

Share the Wealth of Knowledge!

Please share this market update with family, friends, or colleagues. If you would like us to add them to our list, simply click on the "Forward email" link below. We love being introduced!

|

|

|

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Diversification does not guarantee profit nor is it guaranteed to protect assets.

The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of stocks of technology companies and growth companies.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indexes from Europe, Australia and Southeast Asia.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Google Finance is the source for any reference to the performance of an index between two specific periods.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

These are the views of Platinum Advisor Marketing Strategies, LLC, and not necessarily those of the named representative, Broker dealer or Investment Advisor, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer or Investment Advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

|

Robert G. Miller, CFP® , RFC, LUTCF

The Miller Financial Group

7700 West Camino Real

Suite 400

Boca Raton,

FL

33433

561-353-3700

rob@tmfg.com

http://www.tmfg.com

|

|

|