|

S&P 500 at 5-Yr High

Weekly Update - January 14, 2013

|

|

|

In This Issue

|

|

|

|

|

|

The Markets:

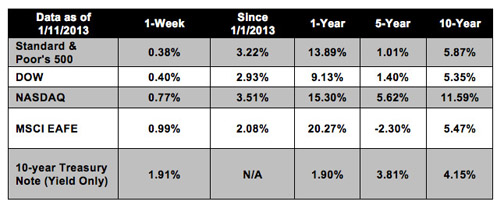

Markets were upbeat last week, closing positive for the second week in a row as traders digested the first fourth-quarter earnings reports and fresh economic data. The S&P 500 was pushed to a new five-year high, gaining 0.38%, while the Dow rose 0.4%, and the Nasdaq increased 0.77%.[1]

The debt ceiling debate is already in swing, with headlines dominated by the idea of minting a trillion dollar coin as a way to sidestep a vote on the ceiling. The comedic suggestion was made in an act of political one-upmanship but isn't a true solution. We hope that with that suggestion out of the way, Congress can get back to its job of making necessary decisions to tackle the deficit and put the U.S. back on firm fiscal ground.[2]

With equities at five-year highs, it's time to start thinking about whether the fundamentals can support further upside. Next week, analysts will turn their attention to a slew of economic reports and more earnings data. According to FactSet Research, S&P 500 companies are expected to report overall earnings growth of 2.4% for the fourth-quarter of 2012. This is much better than the third-quarter's 1% decline; however, much of the growth is expected to come from the financial sector, meaning that other sectors are expected to see growth of just 0.2%.[3]

Perhaps even more important than the data will be the attitude of business leaders about their prospects this year. Their opinions could provide us with an important clue about growth prospects for the U.S. and global economies. Analyst opinions are mixed, as some expect an upbeat outlook from businesses, while others think we'll see more guarded opinions.[4]

Analysts will be also listening closely to Ben Bernanke's first appearance of the year; scheduled for Monday, January 14, 2013 at 4:30 PM. The Fed chairman will be speaking about the economy, and some Fed watchers believe he may discuss a potential end to the Fed's asset-purchase program.[5]

Whichever way markets move in the coming weeks, we'll be paying close attention and seeking out opportunities where they arise. While we're pleased with the way markets have performed thus far, we're always on the lookout for reversals and turbulence, and we strive to build portfolios that can withstand short-term gyrations.

ECONOMIC CALENDAR:

Monday: Ben Bernanke Speaks at 4:30 PM ET

Tuesday: Producer Price Index, Retail Sales, Empire State Mfg. Survey, Business Inventories

Wednesday: Consumer Price Index, Treasury International Capital, Industrial Production, Housing Market Index, EIA Petroleum Status Report, Beige Book

Thursday: Housing Starts, Jobless Claims, Philadelphia Fed Survey

Friday: Consumer Sentiment (preliminary)

|

|

|

|

Performance

Notes: All index returns exclude reinvested dividends, and the 5-year and 10-year returns are annualized. Sources: Yahoo! Finance, MSCI Barra. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not available.

|

|

|

Headlines

Economic growth indicator reaches 18-month high. A measure of future U.S. economic growth rose to its highest level since August 2011, indicating that with fiscal cliff worries behind us, we may have a stronger economy ahead. However, the weekly indicator is volatile, so analysts will be watching future reports closely.[6]

Jobless claims rise, seasonal volatility likely. Despite a rise in jobless claims, details of the report suggest that the job recovery is still ongoing. Jobless claims tend to be very volatile after the holidays as seasonal workers are laid off. However, layoffs have declined and an increasing number of people are voluntarily leaving their jobs - both signs of a healthier job market.[7]

U.S. trade deficit widened in November. A surge of imports led November's trade gap - exports minus imports - to widen 16%, surprising economists who had expected the deficit to shrink. This could point to slowing growth in the fourth quarter for when a country imports more than it exports, cash is pulled out of the economy.[8]

Oil prices fall as China's inflation rises. Oil prices fell Friday as analysts became concerned that China's rising inflation will lead central bankers to rein in stimulus measures, leading to slower growth in the oil-hungry nation.[9]

|

|

|

|

"The ability to concentrate and to use your time well is everything if you want to succeed in business - or almost anywhere else for that matter."

- Lee Iacocca

|

Peanut Butter Pie  This simple, delicious pie is a favorite with kids. Recipe from RealSimple.com. This simple, delicious pie is a favorite with kids. Recipe from RealSimple.com.Ingredients:

1 1/2 cups heavy cream

1 cup marshmallow cream

1 cup creamy peanut butter

9-inch basic flaky piecrust, prebaked

1/4 cup chopped salted roasted peanuts

1/4 cup crumbled chocolate cookies

Directions:

Using an electric mixer beat heavy cream until soft peaks form. Beat in marshmallow cream and creamy peanut butter. Spread mixture into the piecrust and top with peanuts and chocolate cookies. Chill until firm, 4 to 5 hours.

|

|

|

In Hard-Packed Sand, Lose the SW The modern sand wedge has a great deal of bounce (the leading edge is much higher than the bottom of the sole) built into the head of the club. This is engineered to prevent the club from digging too deeply into the sand, and to promote a bounce out of the sand. A problem arises though, when the sand wedge is used on thin, hard-packed sand. The very aspect of the sole that prevents it from digging into soft sand now prevents it from getting under the ball on hard-pack, resulting in thin and bladed shots. These shots will either catch the wall of the trap or will fly low and hot over the green. Go back to the cart and get your gap, lob, or pitching wedge. If you open your stance and your clubface and hit a cut shot, the percentage of success will be higher than if you try to force your sand wedge into doing something it is not designed to do.

|

|

|

Quit Using Antibacterial Soap According to research, antibacterial soaps are no more effective at killing germs and preventing illness than traditional soaps. Consider avoiding soaps containing triclosan, which may contribute to the rise of dangerous, disease-resistant bacteria.

|

Use De-Humidifier Water For Plants Don't throw away lightly used water, such as that collected from a dehumidifier. This gray water is not safe for consumption by people or pets, but it's perfect for watering plants (not edible ones) or for household cleaning when mixed with cleaning agents.

|

|

Share the Wealth of Knowledge!

Please share this market update with family, friends, or colleagues. If you would like us to add them to our list, simply click on the "Forward email" link below. We love being introduced!

|

|

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Diversification does not guarantee profit nor is it guaranteed to protect assets

The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indexes from Europe, Australia and Southeast Asia.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

The Housing Market Index (HMI) is a weighted average of separate diffusion indices based on a monthly survey of NAHB members designed to take the pulse of the single-family housing market. Each resulting index is then seasonally adjusted and weighted to produce the HMI.

The Pending Home Sales Index, a leading indicator of housing activity, measures housing contract activity, and is based on signed real estate contracts for existing single-family homes, condos and co-ops. The PHSI looks at the monthly relationship between existing-home sale contracts and transaction closings over the last four years. The results are weighted to produce the index.

The Chicago Board Options Exchange Market Volatility Index (VIX) is a weighted measure of the implied S&P 500 volatility. VIX is quoted in percentage points and translates, roughly, to the expected movement in the S&P 500 index over the upcoming 30-day period, which is then annualized.

The BLS Consumer Price Indexes (CPI) produces monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services. Survey responses are seasonally adjusted and weighted to produce a composite index.

The Conference Board Leading Economic Index (LEI) is a composite economic index formed by averages of several individual leading economic indicators, which are weighted to produce the complete index.

Google Finance is the source for any reference to the performance of an index between two specific periods.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

These are the views of Platinum Advisor Marketing Strategies, LLC, and not necessarily those of the named representative or named Broker dealer, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

By clicking on these links, you will leave our server as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

|

Robert G. Miller, CFP® , RFC, LUTCF

The Miller Financial Group

7700 West Camino Real

Suite 400

Boca Raton,

FL

33433

561-353-3700

rob@tmfg.com

http://www.tmfg.com

|

|

|