|

|

|

Thinking of Making a Charitable Contribution? Consider This... Thinking of Making a Charitable Contribution? Consider This...

by Brittany Grubbs, CPA, Manager

Charitable giving is a win-win proposition. The charity receiving the gift wins because it is able to use the gift to further its mission. The donor of the gift wins because they get the satisfaction of supporting a cause they care about as well as receiving a tax deduction for their gift. There are a few important considerations when a person is planning their charitable giving for the year.

- There are limits to the amount of charitable contributions you can deduct in a year. Generally, cash donations to 501(c)(3) organizations are limited to 50% of a donor's adjusted gross income (AGI). Some charitable contributions are limited to 20% or 30% of AGI (see http://www.irs.gov/pub/irs-pdf/p526.pdf for additional information related to limits on charitable contribution deductions). Contributions in excess of the applicable limit can be carried forward to a year in which they can be utilized.

- When considering donating stock directly to a charity, it is important to determine whether the stock value has increased or decreased since it was purchased. If the value has increased, it makes sense to donate the stock directly to the charity because the donor will get a deduction equal to the fair market value of the stock on the date of donation and will not have to recognize a capital gain on the disposal of the stock. The deduction of capital gain property (like stock) is limited to 30% of AGI, with any excess contribution carrying forward until it can be utilized. If the value of the stock has decreased, it generally makes more sense to sell the stock and donate the proceeds to the charity so that the donor can recognize a capital loss on the disposal as well as receive a charitable deduction for the donation of the proceeds to the charity.

- Noncash contributions carry some additional substantiation requirements in order to claim a deduction. Generally, when noncash contributions exceed $500, Form 8283 must be completed and attached to the donor's tax return. Depending on the type of noncash contribution made, an appraisal may also have to be completed and, in some situations, attached to Form 8283. Refer to http://www.irs.gov/pub/irs-pdf/i8283.pdf to determine the substantiation requirements related to any noncash contribution you are planning to make.

Charitable contributions are an effective tool in an individual's tax planning strategy. Consult your tax advisor to determine how to be most effective in your charitable giving as well as to ensure you have met all the substantiation requirements to be able to take the deduction for the charitable contribution.

|

|

Are Your Sensitive Spreadsheets Worth More Than $29.95? Are Your Sensitive Spreadsheets Worth More Than $29.95?

by Casey Cox, CPA, IT Support Specialist

Excel is a great tool to organize and keep data. With the password protection feature you can encrypt sensitive and confidential spreadsheets with ease. And you have 100% confidence it's secure, right? Well that answer depends on which file type you are using. The 2003 version of Microsoft Office Suite has a significant security flaw in its encryption, but that was remedied in the 2007 version and up. However, if you are still using the old extension (.xls), then you are still vulnerable to this weakness, which allows anyone that can get ahold of your data to crack the password in a matter of seconds. There are websites out there that provide this service for the low price of $29.95, without even installing software on the computer. The solution is simple, upgrade any .xls files to the newer extension (.xlsx) and use a strong password with a mix of uppercase, lowercase, numbers and symbols. The newer Excel extension uses the same security protocols as most banks. So while nothing is 100% secure, you can be extremely confident your data is protected.

|

|

Do You Drive a Cadillac?

by Tracey Martin, CPA, Partner

Starting in 2018, high-cost employer-sponsored health plans ("Cadillac plans") will be subject to an excise tax as part of the Affordable Care Act. The nondeductible excise tax is 40% of any excess benefit; that is 40% of every premium dollar paid in excess of the annual "high-cost" limit. The ACA's definition of "high-cost" is premiums that exceed $10,200 per employee for self-only coverage and $27,500 per employee for other-than-self-only coverage. The cost is the total amount both the employer and the employee pay in premiums. These baseline dollar limits are expected to be adjusted annually after 2018 based on the application of a "health cost adjustment percentage".

In theory, the Cadillac Tax was meant to target overly generous employer-provided health care plans and lower overall healthcare costs with the projected $80 billion in excise tax collected between 2018 and 2023 helping to pay for the ACA. In reality, with rising health insurance premiums, the tax could impact many more and most employers are already redesigning their plans to avoid it all together. As we have experienced with other components of the ACA, the Cadillac Tax could be changed, delayed or eliminated. However, it is best to plan for it in its current form. If you currently offer employer sponsored health plans that are close to or exceed these dollar thresholds evaluate how the Cadillac Tax will impact your business. As a simple example: - A $14,000 individual plan would pay an excise tax of $1,520 per covered employee

($14,000 - $10,200 = $3,800 * 40% = $1,520) - A $35,000 family plan would pay an excise tax of $3,000 per covered employee.

($35,000 - $27,500 = $7,500 * 40% = $3,000)

If you have questions regarding the tax implications of high-cost employer-sponsored health plans or other sections of the ACA, make sure to consult a tax professional well-versed in the topic.

|

|

|

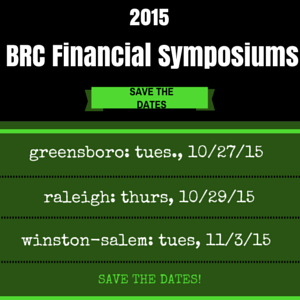

BRC Financial Symposium -

3rd Annual

|

|

|

Bernard Robinson & Company | (336) 294-4494 | pmcmillan@brccpa.com |

1501 Highwoods Blvd, Ste 300

Greensboro, NC 27410 |

|

BRC Strategy is designed to provide information of a general nature and is not intended as a substitute for professional consultation and advice. The opinions and interpretations expressed should not be construed or used as legal or tax advice, written or otherwise, and cannot be used for the purpose of avoiding any penalties that may be imposed under federal, state or local law.

|

|

|

|

|

Copyright © 2015. All Rights Reserved.

|

|

|

|