Email Us

|

|

Overview

The government program established to assist homeowners in distress continues to under perform, with 91,118 trial modifications under the Home Affordable Modification Program (HAMP) being canceled in June and of those more than 70% had been in a trial period for six months or longer.

Based on the June 2010 Servicer Performance Report (Report) issued on July 20, 2010, it appears that, more often than not, most borrowers aren't surviving the trial modification stage.

Servicers also converted 51,205 trials to permanent modifications, approximately 3,481 more conversions than occurred in May. During the same period, the number of trial modifications also increased from May, growing from 30,099 to 38,728.

The recidivism rates for HAMP modifications six months after converting to a permanent modification are 5.9% of HAMP loans are 60+ days delinquent and 1.7% are 90+ days delinquent. At nine months after conversion, the rates rise to 7.7% for 60-day delinquencies and 2.4% for 90+ day delinquencies.

The velocity of the program is slowing down considerably!

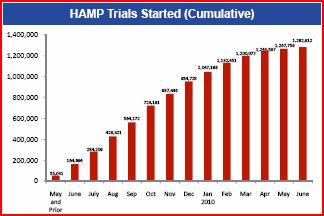

On a cumulative basis, trial modifications started in September-October 2009 were 156,019, but the number of trial modifications in May-June 2010 were 15,753 - about a 90% reduction!

If you have any questions about this matter or would like assistance with mortgage compliance, please contact Jonathan Foxx, Managing Director or call 516-442-3456 x 100. |

Highlights

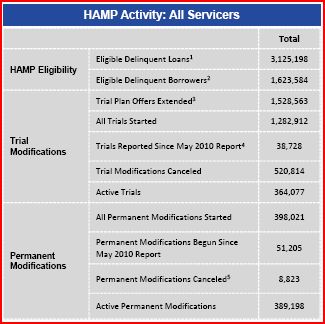

●Number of permanent loan modifications: 346,816 to 389,198 (Increase: 42,382) ●Number of trial modifications canceled: 429,696 to 520,814 (Increase: 91,118) ●Number of "active trials": 467,672 to 364,077 (Decrease: 103,595) These statistics clearly show that the number of failed trial modifications to date are significantly greater than the number of successful, permanent ones, while the number of trials started has dropped precipitously.

|

As indicated above, the velocity of the program is slowing down considerably. On a cumulative basis, trial modifications started in September-October 2009 were 156,019, but the number of trial modifications in May-June 2010 were 15,753 - about a 90% reduction! This is the slowest month-over-month pace since the program began. |

Highlights

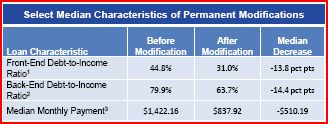

Taken together, the above two charts indicate why trials modifications are probably slowing down: servicers are now pre-qualifying borrowers and are also running out of eligible borrowers. The median front-end DTI before modification is 44.8% (which is about where it has remained for several months); and, the back-end DTI before modification is an astronomically high 79.9% (which, in any event, has been in this high range of 77.5% to 80.2% for several months). That back-end DTI discloses an inescapable fact: nearly 80% of the borrower's income is going to servicing debt - and nearly 63.7% of income even after loan modification - a troublesomely high back-end ratio, which indicates likely defaults in the future.

It's no wonder that many borrowers never make it out of trial modification into permanent modification. Indeed, these are "median" characteristics - so many borrowers have even higher risk profiles! Clearly, the program is not meeting with the kind of success predicted at its inception and is gradually coming to an end. |

Visit Library for Issuance

Making Home Affordable Program

Servicer Report - June 2010 (07/21/10) |

|

Suite of Services and Specializations

Mortgage Compliance Compliance

Administration

Defaults and Claims Reviews Forensic Mortgage Audit®

Mortgage Defaults Task Force Mortgage Quality Control

FHA Examinations State

and Federal Examinations

Mortgage

Due Diligence FNMA|FHLMC|GNMA Applications

Legal Reviews & Remedies Loss Mitigation

Compliance

Sarbanes-Oxley Compliance HMDA & CRA Processing

Mortgage

Fraud Audit Disaster Recovery Plans

CORE Compliance

Matrix® Statutory Licensing

Business Development Information Security Plans

IT

& IS Compliance RESPA-AfBAs

Lenders Compliance Group is the first full-service, mortgage risk

management firm in the country, specializing exclusively in mortgage

compliance and offering a full suite of hands-on and automated services in residential mortgage banking.

We are pioneers in outsourcing solutions for mortgage compliance.

This

communication is sent to our valued clients and colleagues, who

regularly receive our Advisory Bulletins, Mortgage Compliance Updates, Compliance Alerts, and News and Views.

These

publications are free to subscribers. Information contained herein is

not intended to be and is not a source of legal advice.

© 2007-2010

Lenders Compliance Group, Inc. All Rights Reserved. |

|

|

|

|

|

|