|

News and Views

|

Visit Us!

|

|

Overview

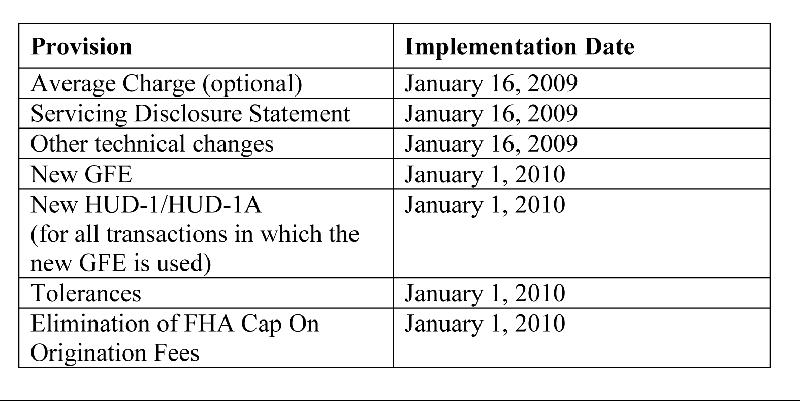

In response to the new RESPA rule that took effect January 1, 2010, the Veterans Administration issued a Circular, on January 7, 2010, that provides guidance on fees and charges a veteran may pay when obtaining a VA guaranteed home loan.

The Circular also announces new documentation requirements for lenders and the elimination of a previously required disclosure statement.

Effective: January 1, 2010.

|

Highlights

NEWLY REQUIRED ORIGINATION STATEMENT

Under the new RESPA rules, there will no longer be a separate line on the HUD-1 called "Loan Origination Fee" to record an origination fee; rather, there is a new line called "Our Origination Charge" that records a combination of the origination fee and the previously itemized fees. Since VA will continue to have a cap on the origination fee and limit the types of charges that may be paid by the veteran, lenders must itemize the fees included in the "Our Origination Charge" line on the HUD-1 Settlement Statement.

Lenders may accomplish this requirement one of two ways.

As described in FHA's Mortgagee Letter 2009-53, available in our Library, if a government program requires that lenders provide more detailed information to specify distinct origination fees and charges, lenders may itemize these charges in the empty 800 lines of the HUD-1 to the left of the column. If there is not sufficient space to itemize all of these fees on the HUD-1, lenders must provide a separate origination statement.

The new origination statement must indicate the purpose of the charge and the amount (Example: Origination Fee - $1,000 and MERS Fee - $15.00). The new origination statement must be signed and dated by the borrower. To ensure that borrowers fully understand the fees being charged, lenders should not split the itemized fees between the HUD-1 and the new origination statement; lenders should use only one of the two approaches to disclose the fees.

Lenders are encouraged to comply with these new procedures as soon as possible; however, all loan applications taken on or after May 1, 2010 must have either the origination statement or a breakout of the origination fees on the HUD-1 as described in the Circular.

|

|

Visit our Library for Issuance

Impact of New RESPA Rule on Fees and Charges - Circular 26-10-01, January 7, 2010

|

|

|

|

Lenders Compliance Group is a full-service, mortgage risk management firm, providing professional guidance to financial institutions in all areas of mortgage compliance.

Specializations

Mortgage Compliance

Forensic Loan Audits

FHA Examinations

State and Federal Examinations

Fannie/Freddie/Ginnie Applications

Mortgage Due Diligence

Legal Reviews & Remedies

Loss Mitigation Compliance

Quality Control

HMDA & CRA Reviews

IT & IS Compliance

Statutory Licensing

This communication is sent to our valued clients and colleagues, who regularly receive our Advisory Bulletins, Mortgage Compliance Updates, Compliance Alerts, Licensing Alerts, and News and Views.

These publications are free to subscribers.

© 2009 Lenders Compliance Group, Inc. All Rights Reserved. |

|

|