|

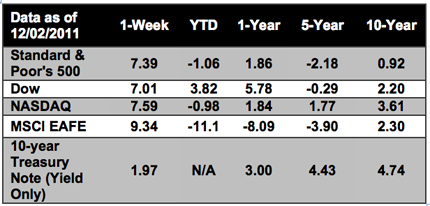

From the worst Thanksgiving week since 1932 [1], to the best weekly gain since 2009, last week illustrated how fickle the stock market can be. The Dow Jones Industrial Average finished up 7% for the week, bouncing back from a 5% loss the previous week on news about... are you ready for it... positive developments in Europe. Take a look at this chart to get a feel for the volatility that we have been experiencing lately.

| | ( Courtesy of thechartstore.com ) |

Now let's go back to the purported reason for the rally - "positive developments in Europe". What exactly were those positive developments?

Basically, several central banks made dollar financing cheaper through swap arrangements, and finance ministers took steps to expand the European Financial Stability Facility. [2] Just as bad news from Europe pushed markets down during Thanksgiving week, good news from Europe pulled markets back up last week. At this point, it should be clear to everyone that we are dealing with highly Europe-charged investor sentiment right now.

In fact, as I have written about before, even the US, through the Fed, is getting into the act.

Fed may give loans to IMF to help euro zone: paper

(http://www.reuters.com/article/2011/12/04/us-eurozone-imf-fed-idUSTRE7B30X320111204)

Think about what they are doing folks. You have a bunch of broke countries borrowing money from each other and then throwing it in the rescue pot as if that will fix the problem. What do I mean? Let's take the US as an example. The US is the biggest contributor to the IMF (International Monetary Fund). Where do we get the money to give to the IMF? We borrow it.

The US spends approximately 40% more than we take in from taxes and fees. So we borrow the rest. We pay the interest on it and give it to the IMF to use. How does that make any sense? Especially when we have our own problems here in this country and will probably need that money here at home.

So does last week's rally mean we're out of the woods and the bulls are back on top? It's possible, but we don't recommend counting on it. Take a look at this headline regarding the two major players in this drama.

Merkel, Sarkozy Seek New EU Treaty to Save Euro

(http://www.moneynews.com/FinanceNews/Sarkozy-Merkel-Eurozone-Plan/2011/12/05/id/419943)

As Bill Engval says, "There's your sign."

While some analysts are expecting stocks to maintain their momentum on the "Santa Clause effect" (Stocks have risen in December nearly four out of five times since 1945, according to S&P Capital IQ, and have risen almost 2% in December after dropping in November - as they did last month), [3] most understand that Europe is still a wild card.

When we see encouraging news and market rallies, it is easy to become excessively positive when we should actually be cautiously optimistic. In the same manner, when we see bad news and steep declines, it is easy to become excessively negative when we should actually be moderately cautious.

What is our point?

In times of uncertainty and volatility, it is particularly critical to stick to a long-term investment strategy that aligns with your personal goals and risk tolerance. And just in case you are wondering, in our opinion, "hang in there, it'll get better" is not a strategy. Simply hoping things will work out is not a strategy.

We encourage you to avoid letting short-term market moves and flashy headlines influence your investment decisions. If you have any questions about whether your current financial plan is still right for you, please feel free to reach out to us. We are always here to help guide you through turbulent times.

ECONOMIC CALENDAR:

Monday - Factory Orders, ISM Non-Manufacturing Index

Tuesday - Bank of Canada Announcement

Wednesday - EIA Petroleum Status Report, Consumer Credit

Thursday - BOE Announcement, ECB Announcement, Jobless Claims, Wholesale Trade

Friday -International Trade, Consumer Sentiment

|