|

|

| |

click to play

|

Featured Video

Gold Ready to Break Out?

Despite turmoil, gold remains in a tight range. So what do the technical indicators tell us? What are the experts saying?

Watch the video as experts discuss whether gold is ready to break out and how to make money in gold using currencies.

|

|

| Dear Readers,

Recent data shows the US economy is slowing down, while stocks continue to rise...

Is there something wrong with this picture?

You bet there is.

It's obvious the market is clearly anticipating another round of QE after Bernanke said last week that the central bank remains "prepared to do more as needed," and reiterated their pledge to keep borrowing rates at record lows through 2014.

The market has been so accustomed to QE that fundamentals in the real world and the market is clearly out of sync.

What I worry about now is a repeat of both 2010 and 2011 where we start the year strong, only to fall back. As with many stocks in this environment, we need momentum to really sustain an acceptable recovery. Right now the numbers are telling us things are slowing down. The labour market is sluggish meaning US unemployment will remain at unacceptable levels for the time being.

Mass manufacturing isn't going to come back to the US. It's that simple. There will need to be a new sector of job creation, or a massive influx of consumer spending, to truly bring unemployment to acceptable levels. I don't see that happening anytime soon.

Corporate Earnings

Corporate earnings are hitting big marks only because profits are being held and not spent. Corporate spending on equipment and software climbed at a 1.7 percent pace, the weakest in almost three years - despite record profits. Although corporate profits recently have hit historic highs, the economy's sluggish 2.2 percent GDP growth doesn't reflect this. That's because profits are being spent overseas.

A recent Wall Street Journal analysis of 35 companies based in the United States that employ more than 50,000 people found that they collectively added 446,000 jobs between 2009 and 2011. But the shocker is that around 75% of them went overseas. During that period, 60 percent of their revenue growth came from overseas. While this means that 334,000 jobs created overseas aren't coming at the expense of the domestic labor market, it clearly shows the real growth and profits aren't coming from the US.

Apple's recent blockbuster earnings? You can thank China's iPhone sales for that.

Still in Charge

So how is the US - especially during an election year - going to show that it will still indeed be the number one driver of the world for years to come? It needs to flex its muscles. The only way it can is to infuse the markets with money.

It's no wonder why Bernanke's comments, combined with the realities of the economy, suggest another round of QE.

Without question, that bodes well for gold and silver - despite manipulation in both markets.

A Dramatic Change in Gold Fundamentals

While the price of gold (dictated by the paper market) has not done much over the past months, the actual physical market is undergoing some extreme demand shift fundamentals.

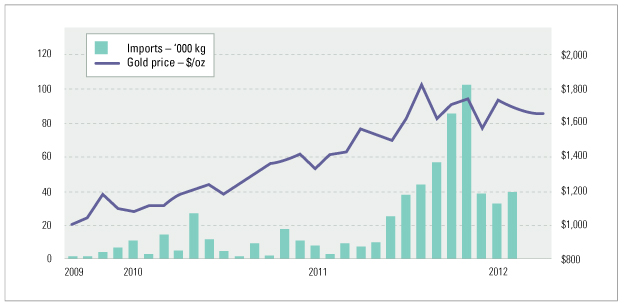

Recent data shows that Chinese gold demand continues to remains strong, with China importing 40 metric tonnes or nearly 40,000 kilos of gold bullion from Hong Kong alone in February. That's nearly 13 times higher than the 3,115 kilograms in the same month last year. Shipments were 72,617 kilograms in the first two months, compared with 10,564 kilograms a year ago or nearly a seven fold increase from the record already levels seen last year.

CHINA'S GOLD IMPORTS FROM HONG KONG

| |

Source: Hong Kong Census and Statistic Dept, Reuters Reuters graphic/Catherine Trevethan, Rujun Shen 11/04/1

|

There's no doubt that the market has missed the importance of the massive increase in the demand for physical gold - the true long term dictator of price.

I have already discussed previously that many countries have begun to increase their physical gold reserves. (see The Hoarding Has Begun)

Last year, central banks purchased 439.7 tonnes of gold. According to the latest IMF statistics, at least 12 countries are known to have increased their gold reserves in March. The stats show that central banks appear to have purchased no less than 58 tonnes in the month. If this continues, that is equal to 696 tonnes per year. I see no reason why they will stop.

In a recent survey of reserve managers at 54 central banks responsible for portfolios worth $6 trillion, almost half the world's total, 71% of them said gold was a more attractive investment than it had been at the start of last year.

If you remember from my past writings, you will know that central banks made their largest purchases of gold in more than four decades last year and have continued to buy the precious metal in the early months of 2012. (see A Record Breaking Event)

Yet gold prices are lower than they were last year. How is this possible? How is it possible that the demand for gold continues to surge, yet prices have dropped?

While it is true that the price of gold can be easily manipulated in the paper markets, the same does not hold true when such a dramatic increase in demand floods the markets. When this happens, who is going to supply that demand? What country is going to give up their gold?

When demand cannot be met, prices will be forced to go much higher. When it does, it will bring a major surge into the overall gold sector. It will make the non-believers, believers.

Gold's True Worth

The question of gold's worth is simple and I challenge anti-gold bugs to deny it. If you have an ounce of gold and you know there are millions of people willing to buy it from you for $2000, would you sell it for $10 because you thought it had no use?

Right now, there are not only people buying physical gold at those prices (i.e. rare gold coins), there are countries.

So gold may not do much but, like art (which is soaring in prices), it's worth what people are willing to pay. And in the not too distance future, those buying gold and silver will be thankful they bought it at a cheaper price.

It know I am arguing my point over and over again in practically every letter I have written in the past few years. But when you have a point of view that opposes the mainstream media and the reckless actions of government policies, you have to do it over and over again until people understand why you think the way you do.

I have chosen to follow in the footsteps of some very brilliant minds who have been right on many of the issues before 2008. They may not have been exact in their timing, but their wisdom and contrarian views have made them a lot of money and preserved a lot of wealth. While we all have our own opinions, our overall sentiment remains the same.

Outstanding investments are only fully recognised after the event.

The End Game

Governments need to monetize their debt. They need people to buy treasuries and bonds. But when the returns on treasuries and bonds fall, so does the money flowing into those investments.

Furthermore, consider that the government must now print and monetize their debt to ensure a stable rise in economic growth and prevent another disaster. As that happens the value of treasuries and bonds is lowered substantially as they become overshadowed by a devaluation of their respective currency through inflation.

That's why the Fed purchased an astounding 61% of the total net Treasury issuance in 2011. The net issuance of Treasury securities is now a whopping 8.6% of gross domestic product (GDP) on average per annum. That's insane. (see A Shocking 2011 Cover-Up)

The mainstream media and the powers behind the suppression of gold and silver prices have effectively driven away your average investor out of the market by the volatile price action. While this may continue, eventually it will be overtaken by the fundamental demand of the physical.

Just imagine if this purchasing power and demand shift in gold were applied to the oil market? What would happen to oil prices if countries around the world decided they wanted an additional 10, 20, or even 30% of the world's production supply?

As I always say, you can't predict politics nor manipulation. But you can't argue with real demand fundamentals.

The demand for gold continues to break records...the price will soon follow.

Until next week,

Ivan Lo Equedia Weekly

Questions?

Call Us Toll Free: 1-888-EQUEDIA (378-3342)

Disclosure: I am long gold and silver through ETF's and bullion, as well as long both major and junior gold and silver companies. It's your money to invest and we don't share in your profits or your losses, so please take responsibility for doing your own due diligence. Remember, past performance is not indicative of future performance. Just because many of the companies in our previous Equedia Reports have done well, doesn't mean they all will.

|

|

W hy I am Excited About This Gold Market hy I am Excited About This Gold Market

After a reasonably long period of sustained and occasionally dramatic escalations, commodity markets in general, and precious metals markets in particular, have declined. This is normal and healthy behavior, even if it is uncomfortable for some market participants. Readers with a long memory will remember the 1970s gold bull market, where the gold price advanced from $35 to $850 per ounce - though in 1975, in the middle of that epic bull market, the gold price declined by 50%. While a 50% decline is a near-religious event for many market participants, particularly those on margin, it is instructive to note that at the bottom of the retrenchment the gold price was up threefold from its $35 low, and that gold went on to increase eightfold in price after the bull market resumed. It is thus important to recognize that cyclical retrenchments are a normal and healthy feature of a secular gold bull market.

Readers should consider whether the reasons for the gold market are intact. Has gold's decline made it more likely that sovereign debts can be serviced or that unfunded obligations can be met? Does it mean that insolvent banks are now healthy? Does it mean that creating trillions of unbacked dollars and euros and renminbi will have no consequences? Of course not. We are simply uncomfortable with volatility.

Gold's Current Weakness

Let's examine some factors that may have contributed to gold's current weakness and think about the probabilities of those factors contributing to further weakening in the gold price.

For the past ten or twelve years, the gold price has been in a steady state of advance. In the near term, some participants probably took some profits, and high prices also probably contributed to demand destruction in industrial fabrication and jewelry demand. A softening of the gold price is likely to reverse the effects of price-induced conservation and substitution, even while investment demand, measured by gold funds and the ETF industry, continues to be strong.

Equity and debt markets appear to be stabilizing as a consequence of quantitative easing in Europe, the US, and China, and the apparent easing of concerns in Greece. This flood of liquidity has forced interest rates down as well as bond and deposit yields, pushing savers into longer durations and riskier instruments - including equities - and lowering servicing costs for debtors, which in turn has lowered perceptions of default risk. The markets appear more confident, and hence gold's attractiveness as insurance is fading. Some of us believe that the root word of confidence is "con," just as I believe the correct phrase for quantitative easing is "counterfeiting." It would appear that in excess of $4 trillion of new currency units have been introduced into the system, with no concurrent increase in underlying wealth in the form of goods or services. This does not make me find gold less attractive relative to fiat currencies or sovereign debt. How about you?

Physical demand in India and Vietnam has been constrained by excise and import taxes on gold in the case of India, and increased regulation in Vietnam. The constraints on physical demand in India has had an important impact on overall gold demand, and has become a hot political issue in India. Gold merchants were on strike concerning the excise tax, further constraining demand. It is worthy to note that South Asian societies have a deep-seated, cultural attraction to gold, and that the fairly recent removal of the taxes they just reinstated was a consequence of widespread smuggling and informal trading in gold. I suspect that central government interference in the Indian gold market will be ineffective and ultimately inconsequential.

Small, commodity-oriented institutions such as hedge funds have experienced strong outflows of equity capital and constrained access to debt financing, which has caused them to engage in forced liquidation of precious metals holdings. This is true, and in my opinion will continue. I believe, however, that if black swan style events destabilize other markets, the gold ETF industry and gold trusts like Sprott Physical Gold will easily absorb the remaining institutional bullion hoards. Further, Sprott has firsthand knowledge of the strong interest among sovereign wealth funds in increasing their bullion holdings.

Gold Equities

Since late 2010, gold equities have underperformed the commodity, and this underperformance has continued, and perhaps increased, as the gold price has declined. These twin trends are uncomfortable to participants in the gold equities markets. Let's examine some of the factors that may have contributed to the underperformance of gold equities relative to gold, and the probable consequence of current market conditions.

It is important to remember that for much of the last decade gold equities outpaced gains in the metals. In fact, the escalations in gold equities pricing became so acute that Canadian analysts were describing companies selling at premiums to their net asset value as "undervalued," because their premium to net asset value (i.e., what they are worth) was less than the industry standard. Always remember, markets work! This prior overvaluation was an important cause of the sector's subsequent undervaluation. The expectations built into gold equities valuations, even relative to gold, were simply unsustainable. In particular, the valuations accorded the junior gold sector were best described as "a bubble in search of a pin." The pin was found. History has shown that markets cure periods of overvaluation; and I suspect that they will also solve this period of undervaluation, relative to bullion, as well.

The emergence of bullion-linked equity instruments like the Sprott Physical Gold Trust and the various Gold ETFs allowed securities investors a new, low-cost, convenient way to participate in the gold markets. These developments at once spurred demand for bullion to back these equity-like instruments and constrained demand for gold equities as investors switched from traditional gold equities to bullion-like equities. I believe this phenomenon was particularly evident as a consequence of the relative overvaluation of gold equities described in the preceding paragraph. Given that the relative attractiveness of bullion-like equities to traditional gold equities was greatest when the gold equities were overpriced relative to bullion, I suspect this attractiveness will lessen now that gold equities are more attractive relative to bullion.

Gold equities were punished, both absolutely and relative to bullion, by their relative corporate underperformance. Many analysts, myself prominently among them, were dismayed at the gold mining industry's abysmal corporate performance during the last decade. The industry's operating cash generation in the face of a gold price escalation from $260 per ounce to over $1,200 per ounce was inexplicably poor. The companies' continued equity issuances in the face of these increases in the gold price meant that existing holders were continually diluted, even as their earnings expectations were always disappointed. Investor fatigue - in fact, investor disgust - was the natural and healthy response to this performance.

Now, even though equities prices continue to decline, corporate performance is increasing, and increasing dramatically. A cursory look at producers' income statements tells a dramatic story: earnings and cash generation, on a per share basis, are rising in dramatic fashion. Capital expenditures are increasingly funded with internally generated cash rather than equity issuances or debt. In fact, even in the face of the gold equities decline, many gold producers are generating cash so fast that even after funding hefty capital budgets, they are able to return cash to shareholders in the form of stock buybacks and increased dividends.

The Juniors

The junior gold industry...

Click Here to Continue Reading

More Casey Research Articles

> So Long, US Dollar

> Doug Casey on Taxes and Freedom

> How to Speculate Your Way to Success: Doug Casey

|

|

| Featured BNN Clip:

Commodities vs. Stocks - Click to Watch

|

|

Upload Your Own Videos - Embed Videos

Is there a video on Youtube or another website that you want to post without uploading it through our technology?

With our new Embed feature enabled, you can now upload and embed any object or video into your blog post. Many of our users are already embedding videos from Fox, Youtube, and CNBC and sharing them with our users.

Embedding is simple. Just copy and paste the embed codes from another website ino the main blog section of your post (not the exceprt).

Where do you find these embed codes?

Embed codes for videos are usually right beside a video.

Here is an example of where the code is on Youtube, highlighted in yellow:

So share what you find with everyone! To learn more, feel free to email or call us at 1-888-EQUEDIA

|

|

Equedia Tips - The Markets Tab

Using the search function at the top right corner of the website, search for any company. Let's use Research in Motion as an example. Once you reach their profile page, click on the MARKETS TAB. You should now see 12 seperate tabs underneath their logo. Try clicking on them and you will find in-depth information such as:

Detailed Quotes - Depth/Level II - Options - Java Charts - News - Profile - Financials - Insiders trades - Filings - Analyst Consensus - Earnings - Historical Data (Highs/Lows, Volumes, Closing/Opening Prices)

|

|

Additional Features (you may not know)

Equedia has many features (you may have overlooked) that will help you manage your investment life and ensure a more enjoyable and useful experience.

Here are just a few of them:

Calendar subscriptions: Keep track of your business events, subscribe to other events, and have access to your online calendar from anywhere in the world. In the near future, we will be working with public companies to add their events to the calendar so that shareholders will never miss an important event again. So call your companies and get them to participate!

Tagging companies to videos and images: Did you know that all of your videos and images can be tagged to public companies? Do you have a video about Google? How about a blog with an image? How about just a blog? Tag it to Google in your blog post, so that anyone searching for Google's quotes and finances can find your coverage!

Buy, Sell, and Hold Ratings: Once you log in, you can submit your buy, sell and hold ratings on the ratings tab so that other shareholders can see what YOU think. You may also access your associates' ratings and see what they think of the shares you hold.

Blog feed subscriptions: Once you add someone as an associate, you will have access to all of their blog posts through your blog feeds. Simply go to your "blog feeds" tab once you log in!

Search function: By far one of the most overlooked but important functions on Equedia. Using the top right hand corner search function, you can find and add any corporations, media users, or investors to your network.

Markets Tab: Under any corporate profile, you will find this tab. Under this tab, you can find the company's news, level 2 depth (delayed), options, charts, profile, financials, insider trades, filings, analyst overviews, earnings, and historical data (these may not be available for all companies)

There are many more useful features on Equedia.com but we think its better if you experience them for yourself. The more associates you have, the more useful Equedia will become for you. So use the new "invite my contacts" function and get started!

|

Forward-Looking Statements

Except for the statements of historical fact, the information contained herein is of a forward-looking nature. Such forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievement of the Company to be materially different from any future results, performance or achievements expressed or implied by statements containing forward-looking information.

Although the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that statements containing forward looking information will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on statements containing forward looking information. Readers should review the risk factors set out in the Company's prospectus and the documents incorporated by reference.

Cautionary Note to U.S. Investors Concerning Estimates of Inferred Resources

This presentation uses the term "Inferred Resources". U.S. investors are advised that while this term is recognized and required by Canadian regulations, the Securities and Exchange Commission does not recognize it. "Inferred Resources" have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of "Inferred Resources" may not form the basis of feasibility or other economic studies. U.S. investors are also cautioned not to assume that all or any part of an "Inferred Mineral Resource" exists, or is economically or legally mineable.

|

|

|

|

|

|

This Week's Most Wanted

The Stock Market's Most Interesting Videos That You Should Watch

|

Companies Under Evaluation This Past Week

|

|

|

|

Disclaimer and Disclosure

Disclaimer and Disclosure Equedia.com & Equedia Network Corporation bears no liability for losses and/or damages arising from the use of this newsletter or any third party content provided herein. Equedia.com is an online financial newsletter owned by Equedia Network Corporation. We are focused on researching small-cap and large-cap public companies. Our past performance does not guarantee future results. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. This material is not an offer to sell or a solicitation of an offer to buy any securities or commodities.

Furthermore, to keep our reports and newsletters FREE, from time to time we may publish paid advertisements from third parties and sponsored companies. We are also compensated to perform research on specific companies and often act as consultants to many of the companies mentioned in this letter and on our website at equedia.com. We also make direct investments into many of these companies and own shares and/or options in them. Therefore, information should not be construed as unbiased. Each contract varies in duration, services performed and compensation received.

Equedia.com is not responsible for any claims made by any of the mentioned companies or third party content providers. You should independently investigate and fully understand all risks before investing. We are not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed and the giving of the same is not to be deemed as an offer or solicitation on our part with respect to the sale or purchase of any securities or commodities. Any decision to purchase or sell as a result of the opinions expressed in this report OR ON Equedia.com will be the full responsibility of the person authorizing such transaction.

Again, this process allows us to continue publishing high-quality investment ideas at no cost to you whatsoever. If you ever have any questions or concerns about our business or publications, we encourage you to contact us at the email or phone number below.

Please view our privacy policy and disclaimer to view our full disclosure at http://equedia.com/cms.php/terms. Our views and opinions regarding the companies within Equedia.com are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect. Equedia.com is paid editorial fees for its writing and the dissemination of material and the companies featured do not have to meet any specific financial criteria. The companies represented by Equedia.com are typically development-stage companies that pose a much higher risk to investors. When investing in speculative stocks of this nature, it is possible to lose your entire investment over time. Statements included in this newsletter may contain forward looking statements, including the Company's intentions, forecasts, plans or other matters that haven't yet occurred. Such statements involve a number of risks and uncertainties. Further information on potential factors that may affect, delay or prevent such forward looking statements from coming to fruition can be found in their specific Financial reports. Equedia Network Corporation., owner of Equedia.com has been paid $5833.33 plus HST per month for 6 months which totals $35,000 plus hst of media coverage on MAG Silver Corp. MAG Silver Corp. has paid for this service. Equedia.com may purchase shares of MAG Silver without notice and intend to sell every share we purchase for our own profit. We may sell shares in MAG Silver Corp without notice to our subscribers. Equedia Network Corporation., owner of Equedia.com has been paid $6666 per month for 6 months which totals $40,000 plus hst of media coverage on Abzu Gold Ltd. and has been granted 150,000 options at $0.20 vesting over a one year period. Abzu Gold Ltd. has paid for this service. Equedia.com currently owns shares of Abzu Gold Ltd. and we may purchase more shares without notice. We intend to sell every share we own for our own profit. We may sell shares in Abzu Gold Ltd. without notice to our subscribers.

Equedia Network Corporation is also a distributor (and not a publisher) of content supplied by third parties and Subscribers. Accordingly, Equedia Network Corporation has no more editorial control over such content than does a public library, bookstore, or newsstand. Any opinions, advice, statements, services, offers, or other information or content expressed or made available by third parties, including information providers, Subscribers or any other user of the Equedia Network Corporation Network of Sites, are those of the respective author(s) or distributor(s) and not of Equedia Network Corporation. Neither Equedia Network Corporation nor any third-party provider of information guarantees the accuracy, completeness, or usefulness of any content, nor its merchantability or fitness for any particular purpose.

info@equedia.com

1-888-EQUEDIA

|

|

|